Incorporating a Sustainable Development Goal Lens in Performance Audits

by Sherazade Shafiq, Director, International Programs, Canadian Audit and Accountability Foundation (CAAF) and Kimberley Leach, Principal, Office of the Auditor General (OAG) of Canada

Introduction

Auditing the Sustainable Development Goals (SDGs) can increase accountability of government for commitments made to the 2030 Agenda for Sustainable Development as well as expedite progress towards achieving these goals.

The global audit community has embraced their role in contributing to Agenda 2030 under the INTOSAI Strategic Plan and shown their commitment specifically through:

- Contributing to conversations at the High-Level Political Forum,

- Developing a robust methodology to audit the implementation of SDGs, i.e., the IDI SDG Audit Methodology (ISAM) and

- Conducting over 130 SDG audits between 2014 and 2023, as illustrated in the SDG Atlas.

This article shares experience from trainings conducted by the CAAF in Canada and abroad. It also draws from experience at the OAG Canada to show how audit offices can take concrete steps to incorporate an SDG focus into performance audits.

Incorporating an SDG Lens into Audits

Audit offices have increasingly wide and complex priorities regarding the audits and activities they undertake. While auditing government commitments and progress toward the SDGs is important, audit offices need some options on how to do this in an efficient and effective manner that fits into existing methodologies and national and international standards.

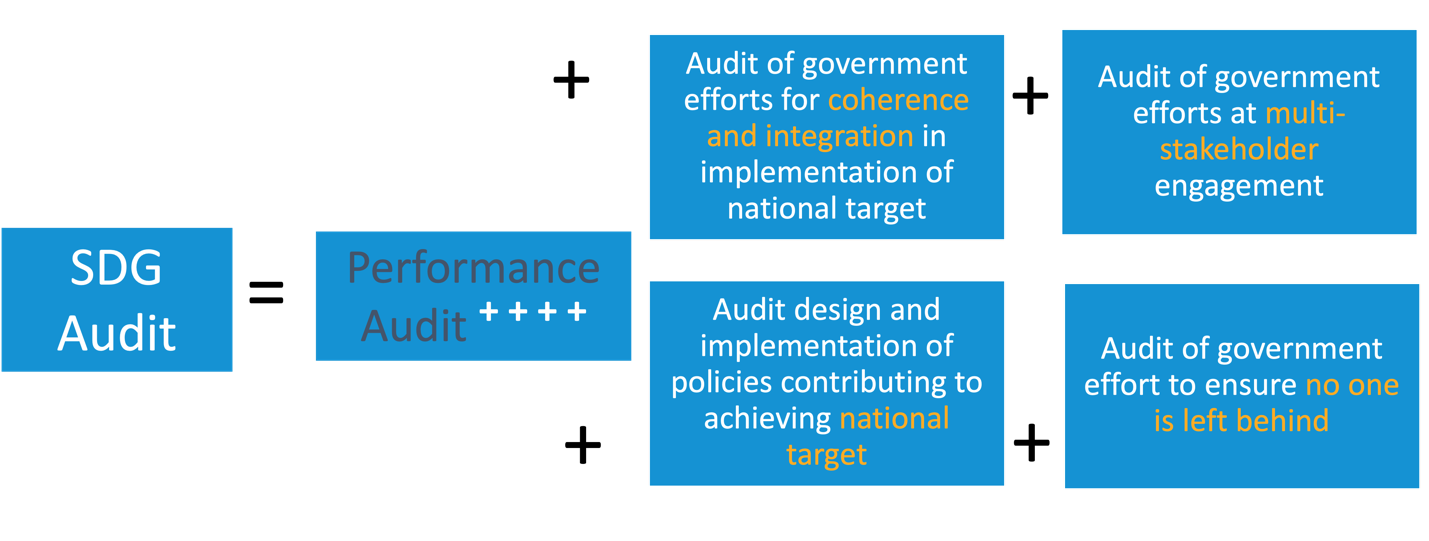

We believe that audit offices can incorporate an SDG lens into most audits and that this does not have to be daunting. We believe that an SDG audit isn’t all that different from a performance audit and that, simply put, a comprehensive SDG audit is just “performance audit ++++” as depicted below:

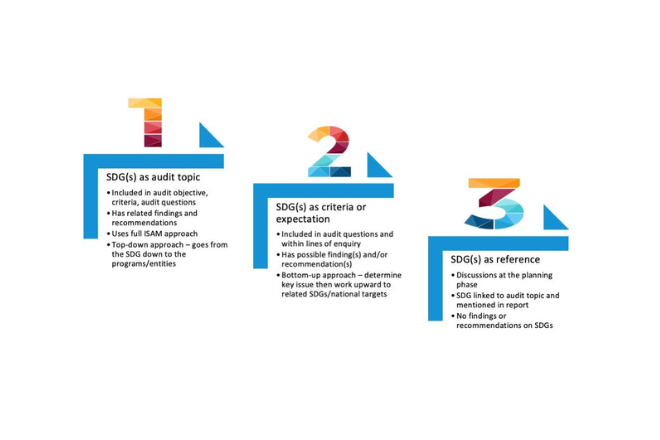

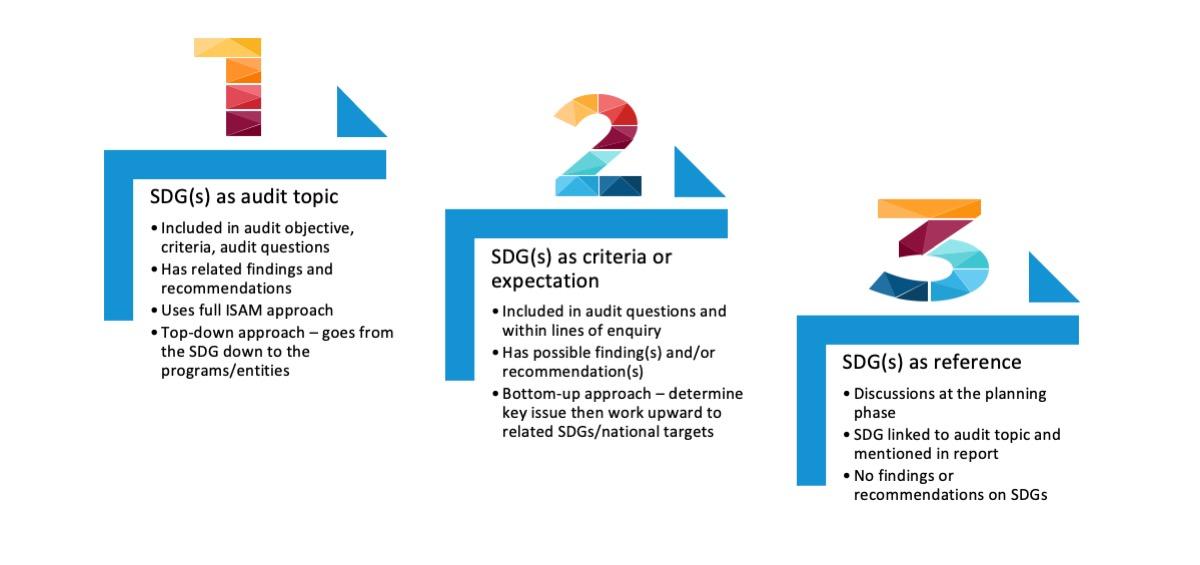

Three Levels of Integrating the SDGs into Your Audits

Applying an SDG lens to your audit can take many forms and can be integrated into existing methodology and standards. We think of three levels of integrating the SDGs into audits. Your performance audit can take the form of a comprehensive SDG audit, which we refer to as Level 1 SDG Integration, or could be at Level 2 or Level 3 as illustrated below:

Level 1 – A full-fledged SDG audit in line with ISAM would consider all four elements below as part of audit scope:

- progress against national targets,

- extent of stakeholder engagement,

- whether the concept of ‘Leave No One Behind’ (LNOB) has been considered in program design, implementation and monitoring and

- extent of policy coherence and integration across levels of government.

This audit would require reference to the national goal as part of the audit objective, availability of data which measures and reports against indicators, comprehensive stakeholder mapping to ensure consideration of key marginalised groups and stakeholders within the audit scope and review of tangential policies adopted by other ministries or other levels of government. As defined by ISAM, the audit would conclude on “the progress made towards the achievement of the national target, how likely the target is to be achieved, and the adequacy of the national target in comparison with the SDG.” For example, see Jamaica’s 2023 audit focusing on SDG 3.d Resilient National Public Health Systems or the OAG Canada 2021 Audit on Implementing UN SDGs which assessed progress toward target 1.2 on poverty reduction; target 5.5 on gender equality in leadership; and target 8.6 on youth unemployment.

Level 2 – At this level, one could start from the key issue to be audited, and then incorporate one or more lines of inquiry or audit questions to support the main audit objective, which address only one, two or three of the above elements. This approach is more bottom up, starting from the key issue as an audit topic, and with SDGs targets and indicators providing possible auditable and results-oriented criteria. For example, OAG Canada’s 2021 audit of Emissions Reduction Fund examined SDG target 9.4 on upgrading infrastructure and retrofitting industries to make them sustainable, while also considering whether the auditee had applied a gender lens.

Level 3 – Since almost all potential audit topics will tie into one of the 17 goals, a link could be made to the audit topic and to the related goal, target and indicator. At this level, a performance audit would not be classified as an ‘SDG audit’ since none of the ++++ are integrated into the audit. But the audit would help to raise awareness of the SDGs and their connection to the audit subject. Auditors should, however, be cautious to avoid ‘greenwashing’ their reports by giving the misleading impression that they have more focus on sustainability than they really do.

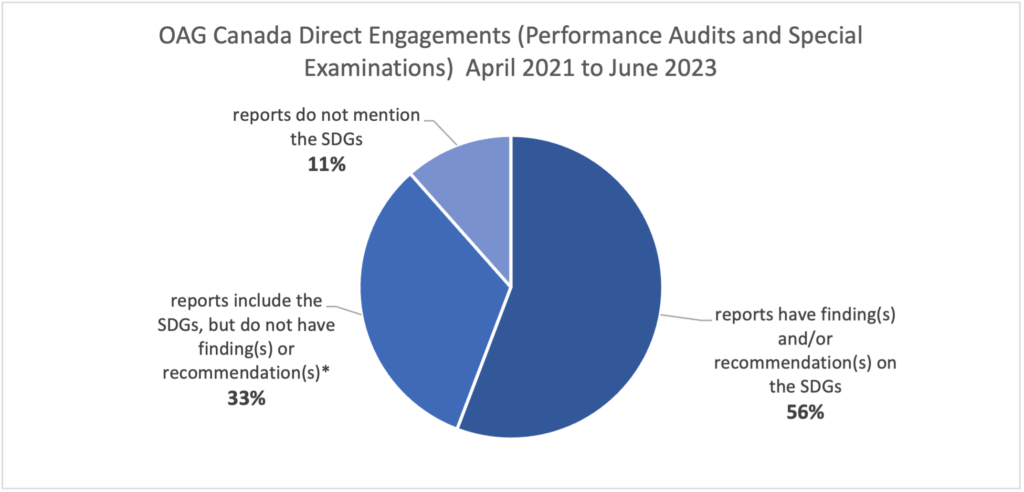

OAG Canada integrates SDGs into all its audits by considering linkages to SDGs early during audit selection and planning. As a result, many performance audit reports include findings and recommendations related to SDG implementation. From 52 total published reports between April 2021 and June 2023, 46 mention the SDGs, and 29 of those have findings and/or recommendations related to SDGs.

*This category includes reports that make no finding(s) or recommendation(s) on the SDGs, but still reference the SDGs somewhere in the report. For example, identifying linkages to the SDGs in a contextual paragraph, using the SDGs as a source of audit criteria, or highlighting the SDGs in the audit scope and approach section.

Top Ten Tips to Start Auditing SDGs.

Based on discussions with many audit offices, we offer the following tips to start auditing SDGs:

- Don’t wait for government to be ready before auditing – At the 2023 High-Level Political Forum, the UN is expected to report falling behind on almost all targets. An audit that identifies gaps in preparedness and frameworks can help expedite government action. While performance auditors often hesitate to audit ‘what’s not there’, SDGs are one of the exceptions to this rule.

- Raise awareness across all levels of government – Don’t assume that everyone knows about the SDGs. Government employees may not even know what their national commitments are, much less consider them in their work. This is particularly relevant at the subnational level. While commitments are made at the national level, they cannot be achieved unless all levels of government are involved. For example, if a federal government is committed to achieving national targets, subnational governments might not be thinking in terms how their activities fit or feed into national targets.

- Involve and educate internal auditors – Internal auditors in line ministries can also apply an SDG lens to their work, allowing much more to be done across government. Don’t try and do it alone.

- Talk to financial auditors – The issuance of the new sustainability standards, means that once these are adopted, sustainability and climate related disclosures will form part of financial statement disclosures. While private sector will lead this, the public sector will also follow suit. SDG targets and indicators are an existing way to provide results focused performance indicators. The UN Secretary General, António Guterres said at a 2020 United Nations Leaders’ Summit that “SDGs could be a ready-made tool to take ESG reporting to the next level”.

- Data will lead the way – Unless disaggregated data is collected, measured and monitored, achieving these goals is like running in the dark and hoping for the best. It is recommended that National Statistics Bureaus are involved in conversations around gathering, maintaining, measuring and reporting data to support achievement of targets and indicators.

- Remember that national targets can and often should be different from the global goals and indicators – When auditors start to consider SDGs, the first misconception is often that countries need to adopt the global goals word-for-word. This is not the case. Ideally, national targets should be customised to make them relevant to the local context.

- Refer to other SDG audits – A review of SDG audits will show you that similar issues crop up. These include issues of policy coherence, lack of structures and poor data frameworks. Focusing on these can save time.

- Use existing structures and systems – Rather than separate and stand-alone consideration of SDGs, build this into existing processes, methodology and templates.

- Keep scope manageable – SAIs sometimes scope SDG audits too broadly. Try limiting the scope to a single target or try limiting the scope to fewer higher risk auditees based on stakeholder analysis.

- Add an SDG lens to your audit topic selection and multiyear planning process – Audit offices consider multiple factors when setting annual or multiyear audit plans. These include auditability (availability of resources, skills and data), potential value-add from the audit, a risk assessment, financial materiality, public interest and importance to parliamentarians. An SDG lens can be applied across these areas. Under risk assessment, consider the progress against linked national targets or incorporation of the concept of LNOB in the program design. Under auditability, consider the availability of relevant national statistics. Under value addition, ensure that environmental, social, and economic areas are covered when selecting topics.

Conclusion

An SDG audit does not have to be daunting. To make an impact, it could be as simple as a regular performance audit, with one or more additional lines of inquiry that address one of the four ‘plusses’ of an SDG audit.

Contacts:

Contact Sherazade Shafiq at sshafiq@caaf-fcar.ca and Kimberley Leach at Kimberley.Leach@oag-bvg.gc.ca for more information about this article.

Additional Resources and Tools:

Learn more about how to incorporate an SDG lens into performance audits.

CAAF resources:

- Sign up for a 2-day workshop on Auditing the Implementation of the Sustainable Development Goals

- Watch our webinars at any time, including Auditing Progress Toward the United Nations’ Sustainable Development Goals and Vaccine and SDG Audits . (Available to CAAF members only)

- Read our Practice Guide to Auditing the United Nations Sustainable Development Goals: Gender Equality

International resources

- WGEA – Key Principles and Tools on Policy Coherence and Multi-stakeholder Engagement for Supreme Audit Institutions

- WGEA – SDGs unfold into targets and indicators which can provide very auditable criteria that are results and outcome oriented – Annex 1 Scoring Matrix

- GAO – Evaluation and Management Guide by the GAO for the identification of fragmentation, overlap and duplication