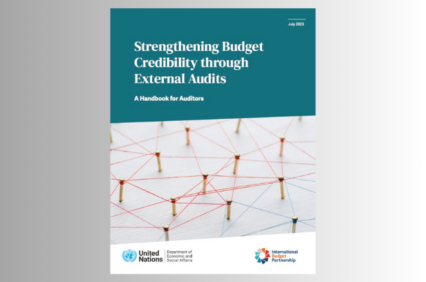

A New Handbook Highlights Ways External Audits Can Strengthen Budget Credibility

Recognizing the significance of budget credibility and the demand for further research and practical guidance on this critical topic, over the last two years Supreme Audit Institutions (SAIs) have collaborated with the Division for Public Institutions and Digital Government of the United Nations Department for Economic and Social Affairs (DPIDG/UNDESA) and the International Budget Partnership (IBP) to develop a handbook for auditors on how their work can contribute to improving budget credibility. The output of this far-reaching effort has been published recently in Strengthening Budget Credibility Through External Audits: A Handbook for Auditors.