SAO Hungary Issues “Pillars of Good Governance” Series

by Prof. Dr. Erzsébet Németh, Editor, Supervisory Manager of the State Audit Office of Hungary

The State Audit Office of Hungary (SAO) fundamentally renewed its activities in the past 5 years further developing international principles of good governance. The SAO’s study series titled “Pillars of Good Governance” and the Hungarian model of good governance embody the results of our work, our experience gained during the renewal and the synthesis of our knowledge.

In accordance with its institutional strategy, the mission of the State Audit Office of Hungary (SAO) is to promote the transparency and regularity of public finances with its value creating audits performed on a solid, professional basis, thus contributing to “good governance”. By now, good governance has become a concept that can be described with a complex set of criteria against which the performance of individual economic policies and state organizations can be measured.

Supreme Audit Institutions (SAI) are important components to good governance. From our point of view, SAIs are the most important institutions of good governance.

The Role of SAO in Good governance—The Hungarian Model

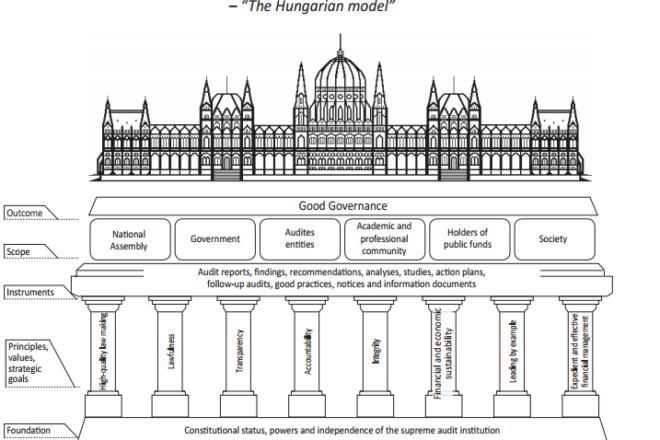

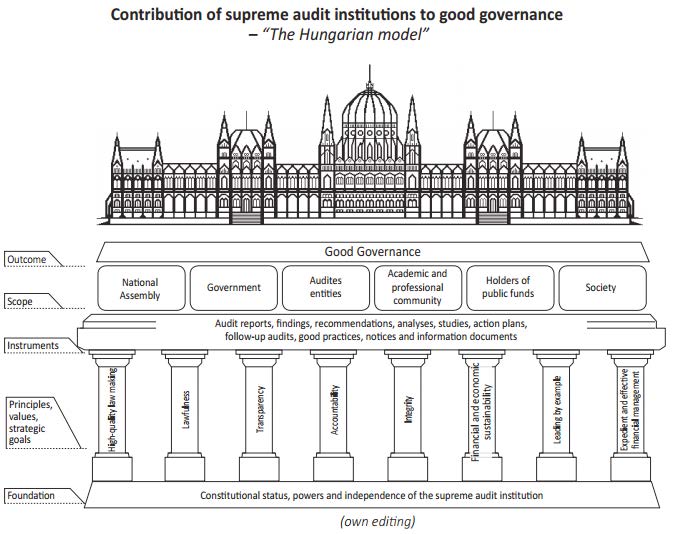

In consideration of its mandate and the duties enshrined in the new legislation, the SAO of Hungary has constructed a model to provide an overview and a classification of the contribution of SAIs to good governance. The Hungarian model (Figure 1) presents the basic conditions, principles, tools and scope of influence associated with the promotion of good governance. Prior to this model, the role of SAIs in supporting good governance have not been explained by means of a similarly comprehensive model.

First level: Foundations

Just as INTOSAI’s founding principles and core principles, the constitutional status and independence of the SAI establishes the cornerstone of the Hungarian model, ensuring the model institution delivers objective, unbiased findings and independently selects its audits and methods—all in an effort to ensure effective good governance.

Second Level: Fundamental Principles and Goals

Moreover, the Hungarian model determines the fundamental principles and strategic goals (second level) that serve as a compass for SAIs in supporting good governance, including the definition of objectives, selection of audited entities, planning of individual tasks and evaluation of the results. Pillars for SAIs in supporting good governance, according to the Hungarian model, are the following:

- high-quality lawmaking;

- lawfulness;

- accountability;

- transparency;

- integrity;

- economic and financial sustainability;

- a model organization; and

- reasonable and effective financial management.

Third Level: Instruments

The next level of the model enumerates the tools that SAIs can rely on in their efforts to support good governance. SAIs exercise their influence by issuing reports, findings, recommendations, analyses and studies; requesting and evaluating action plans; performing follow-up audits; sharing good practices and audit experiences; issuing notices and administrative indications; preparing information documents; publishing opinions; and actively engaging in social and professional communication.

Fourth Level: Scope of Influence

At the fourth level, the model illustrates the ways in which SAIs impact institutional, professional and social groups by leveraging the tools available to them in order to support a well-managed state. These are:

- the National Assembly and the Government;

- the audited entities;

- all organizations that use public funds, and, hence, are in a position to utilize the audit findings and recommendations of SAIs;

- academic and professional audiences, and

- society at large, in particular, the community of taxpaying citizens.

Fifth Level: Outcome

According to the Hungarian model, the outcome is good governance itself. The purpose of our activity is to ensure high-quality lawmaking, strengthen lawfulness, spread integrity-based operations, promote good practices of the SAI, improve the transparency of public spending, strengthen economic and financial sustainability and stability, increase audit coverage and accountability and implement reasonable and effective financial management. We can only consider our work effective if a measurable step forward has been made in respect to the above aspects.

The model not only provides a theoretical framework for the activities of SAO supporting its own good governance, but it may also provide a guideline for defining coherent international requirements.

A Study Series—The Synthesis of Knowledge of the SAI

The promotion of good governance and knowledge transfer has gained an increasingly important role within the SAIs. It can be said that, in recent years, each activity of the SAO of Hungary has been permeated by an approach facilitating good governance, exerting influence on a wide array of activities, such as audits and their utilization, the importance of analyses and studies; and efforts aimed at fostering the integrity of the public sector.

A series of individual studies entitled, “Pillars of Good Governance–Focus on the State Audit Office of Hungary as a Supreme Audit Institution,” presents the role of SAIs in the promotion of good governance in an international comparison; defines the criteria, principles, requirements, instruments and scopes of influence of good governance; and gives an account on how the requirements on the support of good governance were fulfilled at the SAO of Hungary.

The Study Series (see Figure 2), considered one of the most important intellectual products of SAO in the past five years, consists of 11 individual studies. These interlinked works present the activities from the angle of SAO’s auditing, consulting and analyzing functions, as well as the linkage to good governance. The studies, detailed below, form a single volume (or manual).

- The Supreme Audit Institutions’ Contribution to Good Governance

- Cornerstones of Supporting Good Governance

- Contribution of the State Audit Office of Hungary to the Quality of Legislation

- Audit and its Utilization at Auditees

- Transparency of Public Finance Management

- Establishing the Culture of Integrity in the Hungarian Public Sector

- Guarding Budget Sustainability

- Supporting Good Governance in Audit Planning

- Value Creating and Construction—Renewal of the organization and operation of SAO

- Supporting the Effectiveness of Good Governance

- Renewal of Public Management

The individual studies within the series are published both in Hungarian and English in the form of working papers, and are available electronically at https://www.asz.hu/en/publications/pillars-of-good-governance.