by Hasan Masud, Pakistan Audit and Accounts Service, Office of the Auditor General of Pakistan

Quality—An Introduction

“A major challenge facing all Supreme Audit Institutions (SAIs) is to consistently deliver high quality audits and other work.”—International Standards of Supreme Audit Institutions (ISSAI) 40, “Quality Control for SAIs.”

Quality, the degree to which inherent characteristics—clarity, effectiveness, efficiency, objectivity, relevance, reliability, significance and timeliness—of an audit fulfills requirements, must be viewed as a continuous process, one that occurs throughout the audit cycle.

Controlling and assuring quality can be challenging, particularly in environments where resources are limited, since quality involves systems and processes aimed at ensuring SAIs issue reports that are appropriate and in accordance with applicable laws and regulations. Creating a central, dedicated quality office is essential—it allows a SAI to focus on the public expenditure cycle in its entirety, improve final reports prior to issuance, and creates a more effective and efficient framework.

Managing Quality—SAI Pakistan’s Experience

Pakistan’s SAI is at the heart of the nation’s accountability process. Led by an Auditor General serving a fixed, four-year, non-extendable term and staffed with more than five thousand employees in 30 field audit offices across the country, SAI Pakistan performs nearly nine thousand audits annually.

The audits and financial recovery efforts have proven successful, in part, due to a strong quality management system based on strengthened ethics, standards, guides and frameworks.

SAI Pakistan has adopted the International Organization of Supreme Audit Institutions (INTOSAI) code of ethics, and SAI Pakistan’s Financial Audit Manual (FAM), Quality Management Framework (QMF) and public sector audit guidelines are consistent with the ISSAIs.

The FAM. The FAM provides auditors with a set of modern, ISSAI-based standards, concepts, techniques and quality assurance arrangements for auditing government entities in Pakistan. A comprehensive document spanning the audit cycle, the FAM requires the SAI to pay particular attention to quality assurance programs as a means to improve audit performance and results.

Establishing systems and procedures to confirm integral quality assurance processes have operated satisfactorily; ensure audit report quality; and secure improvements while avoiding repetition of weaknesses are part of the FAM’s provisions. The SAI has implemented a system of quality assurance checks and balances that are objective and consultative and include periodic reporting to top management.

The QMF. In Pakistan, an audit report tabled before the Public Accounts Committee (PAC) passes through several quality control and assurance stages, which includes team observations and field office report re-examination prior to sending forward to the Auditor General, who also provides a thorough analysis prior to report finalization.

The QMF, originally implemented in 2011, was developed using INTOSAI and Asian Organization of Supreme Audit Institutions (ASOSAI) standards and guidelines.

The framework provides three broad mechanisms to ensure quality:

- Quality Assurance (QA) is implemented by the head of a particular field audit office and focuses on quality throughout the audit (at the onset of audit planning through audit execution to audit report production).

- Quality Control (QC) is the application of external quality checks on an audit office. It takes place in two stages: (1) sample testing an audit office’s previously quality-assured assignments; and (2) examining all Quality Control Committee (QCC) final audit reports.

- Quality Improvement includes creating and implementing corrective actions based on quality assurance and quality control reviews.

To ensure QMF compliance, SAI Pakistan established two committees—an internal QCC (headed by a Deputy Auditor General (DAG) in the audit’s department) and an external QCC, led by a DAG outside the department performing the audit.

Managing Quality—Some Challenges

Today, SAIs operate in a constantly changing world with an ever-rising tide of expectations for transparency and accountability. Quality Management (QM) must be viewed as a dynamic process aimed at responding to these changing societal demands. Some current challenges faced by SAI Pakistan include:

- Treating QM as a rotational assignment;

- Developing a proper Information Technology (IT) support system;

- Missing linkages with Civil Society Organizations (CSOs);

- Developing and managing relationships with auditees;

- Managing organizational change;

- Sustaining reforms;

- QM training;

- Retaining talent; and

- Expanding areas of operation.

Managing Quality—Some Recommendations

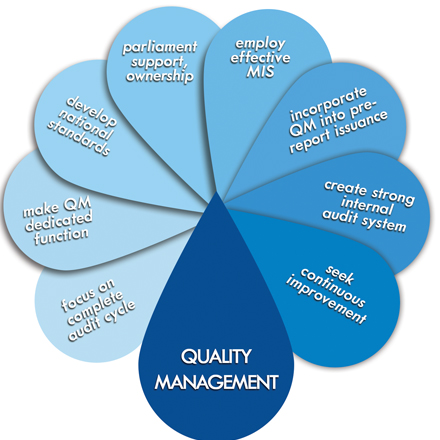

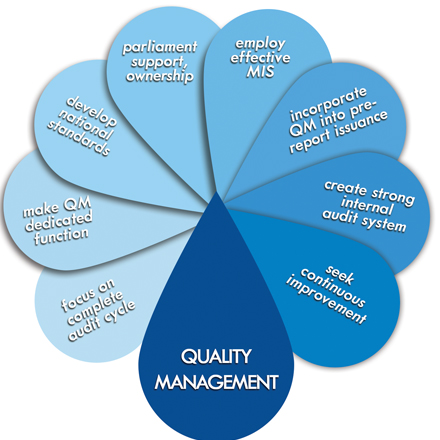

- Focusing on the Complete Audit Cycle. Creating high standards for reports is key, as is emphasizing overall quality. To do this, the quality cycle must begin at the pre-audit stage and end when final recommendations are implemented at the PAC level.

- Making Quality Management a Dedicated Function. An independent office dedicated to managing and assuring quality provides more consistent, institutional approaches to quality. This notion can be further strengthened through training that makes quality management an automatic, continual part of the audit process.

- Developing National Standards. SAI Pakistan is finalizing a Performance Measurement Framework (PMF) draft report, which represents a critical first step in consolidating the SAI’s various frameworks while also conforming to ISSAI guidelines. This effort can lead to future national public-sector auditing standards development.

- Parliamentary Support and Ownership. SAI Pakistan and its quality framework operate within limits defined by parliament. It is important that parliament and the PAC ensure no financial, administrative or legal issues limit the SAI’s scope in producing high-quality reports.

- Employing an Effective Management Information System (MIS). An MIS supports QM frameworks by providing a platform for report centralization, control, filtering and processing. For example, a robust MIS can facilitate report prioritization by flagging important issues and sensitive observations.

- Incorporating QM into Pre-Report Issuance. The QM intervention must be a pre-report issuance inspection, not a post-report inspection step. Adequate, competent staff across fields (audit, IT, administrative) is imperative.

Creating a Strong Internal Audit System. Establishing an independent internal audit department (and improving coordination with external audit divisions) at the federal and provincial levels is vital to broadening audit quality.