Financial Audits and Mechanisms for Good Governance of Public Funds: Promoting Accountability, Transparency, and Citizen Trust through Oversight and Best Practices

Author: May Al-Roomi – Senior Information Systems Auditor – State Audit Bureau of Kuwait

Introduction

Good governance depends on the efficient and transparent management of public funds. Financial audits and oversight mechanisms have become increasingly important as public trust is closely tied to financial accountability. These audits and mechanisms have two main purposes: detecting and preventing corruption and mismanagement, as well as promoting transparency and strengthening institutions to deliver tangible benefits to citizens.

This article reviews the technical and practical issues of financial audits and other mechanisms of governing public funds. It discusses the best practices in public sector financial auditing, the role of audits in fighting corruption, and the frameworks that support accountability. It also provides examples of how financial audit processes can enhance governance and the welfare of the citizens.

The Role of Financial Audits in Public Sector Governance

Financial audits can be defined as systematic evaluations of public financial statements and operations to determine compliance with legal requirements, regulatory standards and ethical principles. These audits help the public sector achieve the following objectives:

- Verification of financial reports for accuracy to maintain their integrity.

- Minimization fraud, mismanagement and malpractice by ensuring close inspection of financial operations.

- Better guidance for financial decision-making, leading to enhanced resource allocation.

- Support for transparency by allowing public access to audit results.

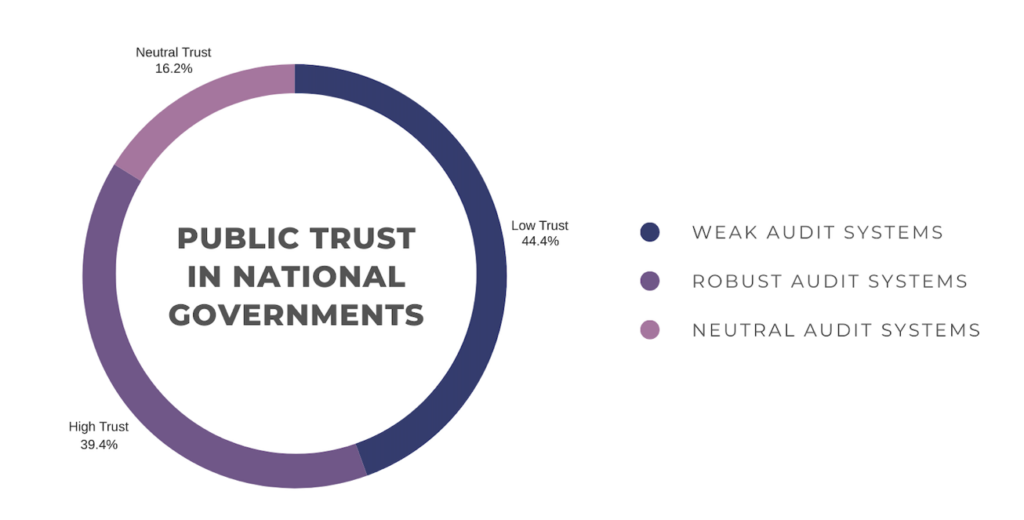

The Organisation for Economic Co-operation and Development (OECD)’s 2024 Survey on “Drivers of Trust in Public Institutions”, together with other studies, demonstrate that public trust in government directly relates to transparency and accountability measures. Strong financial auditing systems function as a key element among these measures. The data presented in Figure 1 demonstrates that nations with effective auditing systems maintain stronger public trust levels, but systems with weak auditing approaches tend to produce lower trust scores.

Supreme Audit Institutions (SAIs) along with national audit offices should perform independent audits on government entities. The executive branch must remain separate from these institutions because such independence ensures the objectivity and credibility of their audit work.

Best Practices for Conducting Public Sector Financial Audits

The following best practices should be implemented to maximize the impact of financial audits:

- Adherence to International Standards

The public sector needs to adopt International Standards of Supreme Audit Institutions (ISSAIs) from INTOSAI, as these standards offer direction for audit planning, execution, reporting and follow-up activities to establish consistent and credible auditing practices.

- Risk-Based Audit Planning

Auditors should direct their audit efforts toward areas with the highest risk levels instead of using uniform procedures for all cases. For example, an auditor could apply more scrutiny toward large procurement contracts, infrastructure projects and grant distributions, as these areas present higher risks of mismanagement or irregularities.

- Timely and Accessible Reporting

Unrestricted access must be provided to audit reports, which must be released promptly. Clarity of such reports should be improved through executive summaries and visual data to help non-technical stakeholders better comprehend the information.

- Stakeholder Engagement

Auditors should attend meetings with legislative bodies, civil society groups and media representatives to explain their findings and to encourage public discussions regarding audit results. This fosters accountability and extends the impact of audits beyond technical circles.

- Robust Follow-Up Mechanisms

Audits should not end with a report. SAIs must create monitoring systems to continuously track audit recommendations through performance metrics and defined timelines.

Auditing as a Tool to Combat Corruption and Financial Mismanagement

Corruption and financial mismanagement deplete public resources, damage public trust and hinders development. Financial audits function as the first line of protection against such threats by performing their fundamental roles which include:

- Detecting Irregularities: Audits detect financial record anomalies which include misstatements and unauthorized expenditures and weak internal controls. The identification of such issues results in additional investigations, possible prosecutions and reform actions.

- Strengthening Internal Controls: Audit recommendations often suggest improvements to internal control systems, including segregation of duties, enhanced documentation, and proper authorization processes, all of which reduce opportunities for fraud.

- Encouraging a Culture of Integrity: Over time, the consistent application of audits instills a culture of accountability across public institutions. Employees demonstrate greater caution and diligence because their work activities can undergo independent evaluation and internal reviews.

- Supporting Legal and Disciplinary Action: Audits which reveal illegal activities allow for legal consequences and administrative penalties to be applied. This reinforces the rule of law and signals zero tolerance for abuse of public office.

Mechanisms and Frameworks for Accountability in Public Fund Management

Financial audits serve their purpose best when they operate within an extensive governance framework. The following mechanisms and frameworks should operate alongside financial audits to establish accountability:

- Public Financial Management (PFM) Systems: The Public Financial Management (PFM) systems include budget planning, execution, accounting, and reporting. Real-time public expenditure data from an integrated PFM system allows for more efficient and accurate audits.

- Legislative Oversight: The authority to review audit reports together with the power to summon officials and enforce corrective actions should be given to parliaments and audit committees. Such measures will enhance accountability while reducing instances of misconduct.

- Transparency Portals: Displaying real-time government expenditure on digital platforms enhances both public oversight and trust. The data enables citizens together with watchdog organizations and journalists to maintain government accountability.

- Whistleblower Protections: Internal mechanisms which allow financial irregularities to be reported anonymously by insiders play a vital role. Whistleblowers frequently serve as the initial source of misconduct detection, and their protection mechanisms boost reporting rates.

- Civil Society Participation: National organizations, advocacy groups and academia play a vital role in interpreting audit findings, educating the public, and pushing for reforms.

- Implementation and IT-Enabled Monitoring Mechanisms: Digital tools and systems provide an effective method to implement governance frameworks. Such tools and systems allow for accurate reform tracking through error reduction and data consistency while offering real-time oversight capabilities. The combination of PFM systems with transparency portals and audit processes creates better accountability while supporting continuous improvement.

Case Studies: The Impact of Effective Financial Audit Processes

- Saudi Arabia: General Court of Audit’s Digital Transformation

Dr. Hussam Alangari, President of the General Court of Audit of Saudi Arabia (GCA) led the GCA through a major transformation to boost its auditing capabilities. The GCA launched the “Shamel” electronic auditing platform, which integrated artificial intelligence (AI)-based audit methods with data analytical tools. The digital transformation enabled real-time data access while improving communication between the GCA and audited entities and strengthened financial oversight to meet Saudi Arabia’s Vision 2030 targets.

- Kuwait: Strengthening Auditor Independence through IT Governance

A 2023 study investigated how Kuwaiti Islamic banks are improving the independence of external auditors through the implementation of strong information technology (IT) governance frameworks. The banks have established clear IT policies and obtained departmental commitment and standardized metrics to create an environment that supports objective and independent auditing practices. The study established that IT governance measures play a substantial role in enabling auditors to work independently which leads to better financial audit quality and reliability in the Kuwaiti banking sector.

- Qatar: AI-Augmented Oversight in the Qatar Financial Centre Regulatory Authority

The Qatar Financial Centre Regulatory Authority (QFCRA) has adopted artificial intelligence in its supervisory and financial oversight functions. The authority employed AI-augmented decision-making tools to improve the monitoring of financial entities, to expedite regulatory compliance reviews, and to enhance the accuracy of risk assessments. This change is in line with Qatar’s strategic move towards data-driven governance, financial integrity, and the implementation of technology in proactive audit supervision.

Challenges and Opportunities

Financial audits encounter multiple obstacles despite their multiple advantages, such as the following:

- Audit institutions in developing countries suffer from lack of trained staff and inadequate tools.

- Political interference and lack of independence that undermines the credibility and effectiveness of audits.

- Weak enforcement of audit recommendations because there are no adequate follow-up mechanisms in place.

- Public engagement is restricted in certain areas because people are unaware about audit reports and how to use them to enforce accountability.

Supreme Audit Institutions (SAIs) encounter these recurring obstacles which reduce their operational effectiveness. The most frequently encountered problems are shown in Figure 2 which includes insufficient staff, political interference and inadequate follow-up systems.

Several solutions can address these challenges, including:

- Utilizing advanced tools that implement AI and data analytics to improve audit planning, risk detection and fraud analysis.

- International cooperation with audit institutions and donor agencies, which enables the development of capacity building.

- Performance improvements through peer assessments and benchmarking processes.

- Leveraging technology and modern mobile applications to enable real-time financial oversight.

Conclusion

Financial audits that follow best practices and operate transparently serve as essential tools for promoting good governance of public funds. Such auditing processes enable institutions to protect their resources while revealing inefficiencies and preventing corruption. Public engagement combined with modern technology and robust oversight frameworks makes these audits more effective drivers of accountability.

References

- ISSAI 100: Fundamental Principles of Public-Sector Auditing. https://www.issai.org/pronouncements/issai-100-fundamental-principles-of-public-sector-auditing/

- ISSAI 200: Financial Audit Principles. https://www.issai.org/wp-content/uploads/2020/12/ISSAI-200-Financial-Audit-Principles.pdf

- ISSAI 300: Performance Audit Principles. https://www.issai.org/pronouncements/issai-300-performance-audit-principles/

- ISSAI 400: Compliance Audit Principles. https://www.issai.org/pronouncements/issai-400-compliance-audit-principles/

- INTOSAI Official Website. https://www.intosai.org/

- OECD Public Integrity Handbook. https://www.oecd.org/en/publications/oecd-public-integrity-handbook_ac8ed8e8-en.html

- OECD Public Integrity Indicators. https://oecd-public-integrity-indicators.org/

- OECD (2024). Survey on the Drivers of Trust in Public Institutions. https://www.oecd.org/gov/trust-in-government.html

- INTOSAI Development Initiative (2020). Global SAI Stocktaking Report. https://gsr.idi.no/gsr2020

- Wikipedia (2025). Hussam bin Abdulmohsen Alangari. https://en.wikipedia.org/wiki/Hussam_bin_Abdulmohsen_Alangari

- Hossain, I. (2024). Transition to AI-Augmented Decision-Making in Financial Supervision: Case Study in Qatar Financial Centre Regulatory Authority. https://aaltodoc.aalto.fi/items/1ab74b73-c3b1-41c0-8249-e5f3a2e8f056

- The Impact of Applying Information Technology Governance in Kuwaiti Banks to Realize the Independence of the External Auditor. https://www.researchgate.net/publication/376666203_The_Impact_Of_Applying_Information_Technology_Governance_In_Kuwaiti_Banks_To_Realize_The_Independence_Of_The_External_Auditor