Impact of Government Use of Trusts and Funds on Financial Accountability: The Manitoba Experience

Author: Yves Genest, Senior Advisor, Project Audits, Office of the Auditor General of Manitoba

Introduction

Governments at a global level, can create various financial structures to segregate funds, set aside funds for specific objectives and manage funds on behalf of other parties. These structures can take the form of various types of trusts, funds, and special-purpose accounts. Although they provide alternative financing mechanisms that are advantageous in certain circumstances, they can also present challenges from an accounting and auditing perspective.

This article explores considerations, impacts and ramifications of the use of such mechanisms by examining the use of trust accounts by the Manitoba Provincial Government (the Province). In particular, audits undertaken by the Office of the Auditor General of Manitoba of the partnership between the Province and Winnipeg Foundation (WF) provide a useful lens to examine these issues.

Case Study: The Winnipeg Foundation

In 2018, the Province created four new trust accounts at the Winnipeg Foundation, to support various program initiatives. It is part of a complex structure of recipient organizations, with several layers of separate funds flowing into each other, falling under the term community foundations. Since 2018, $410 million has been allocated from the Government Reporting Entity (GRE) to community foundations in Manitoba. Most of these funds are to be held in perpetuity by these organizations. (OAG Manitoba, 2019) and (OAG Manitoba, 2021)

For example, each WF fund or trust account is initially created with a transfer from the Province. In most cases, the initial transfer is in the form of an endowment—a large deposit, which will earn investment income that will then be used for a specific purpose. In some cases, the income goes back each year to the Province or to a controlled entity of the Province to use for a specific purpose during that year. In other cases, the funding flows from WF to an entity outside of the Province’s control to be used for a specific purpose.

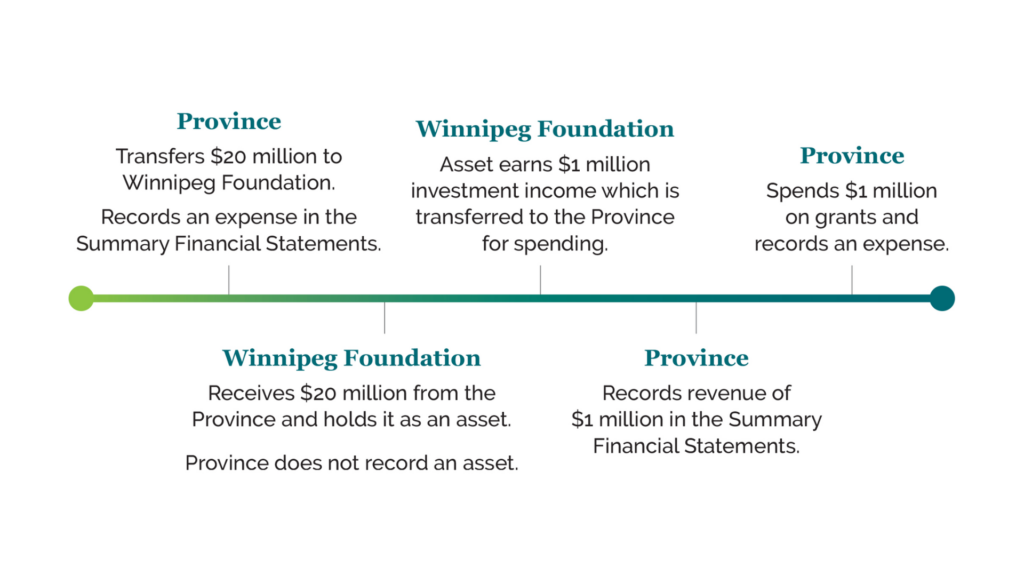

To illustrate how transfers to WF could be accounted for, a description of a hypothetical $20 million transfer is provided in the diagram below. It should be noted that is only one of several other funding variations, one of them being that the money doesn’t flow back (OAG Manitoba, 2021)

Advantages of using trusts and special-purpose funds

Using trusts and funds as funding vehicles can help achieve policy objectives. They can be attractive options for government decision-makers because they provide some advantages. One of them is a guaranteed, recurring funding source for the programs covered. Like many other public administrations, the Province requires that any resources (money) not used by a department during the year will lapse and cannot be spent in the next fiscal year (Government of Manitoba, 2025). An irrevocable trust account avoids this constraint.

Also, the long-term impact on the annual surplus or deficit, could be considered advantageous because the long-term funding provided for a specific purpose will cause a one-time increase to the deficit or reduction in the surplus. After the fund is set up, there is no impact on net annual surplus or deficit. (OAG Manitoba, 2021)

It is also claimed that the formula adopted by the Province, by delegating the attribution of grants in many instances, is a more efficient (Congressional Research Service, 2025) and effective (Person, A.E., 2009) way of managing them. The foundations can establish their own allocation mechanisms and have more built-in knowledge of the needs of the communities and of the type of interventions that will generate the most successful outcomes.

Potential downsides of using trusts and special-purposes funds

Because such funding mechanisms deviate from the usual budgetary processes, the Province must take into account issues and impact considerations, through discussions, approvals and controls. There are obvious concerns regarding accounting provisions and mechanisms that should be used to provide an adequate treatment of these transactions in financial statements. Among the issues that should be considered, OAG Manitoba outlined the following (OAG Manitoba, 2021):

- Significant expense in the first year: Utilizing trusts and special purposes funds reduces the impact on future years’ annual results. However, the impact to the financial statements in the first year is much higher compared to a scenario where the Province chose to fund these programs each year.

- Control: The approach used for WF funds removes control from the Province and as a result, the assets were not included in the financial statements. It also removes the Province’s unilateral authority to use these funds for other purposes in the future. As previously indicated, this approach provides a guaranteed funding source for these programs and their objectives. However, the Province has lost flexibility with these funds and cannot use them for a different purpose if priorities change in the future.

- Cost of the structure: If these funds are being set up when the Province is in an annual deficit position, it means that they are being funded by increases to borrowings.

Using the Synergy Between Performance Audits and Financial Audits

From a financial accountability standpoint, the core issue is related to the control of the funds. Although these funds are treated as gifts, they remain public funds spent to benefit citizens, and therefore assurance must be provided to ensure that they are achieving their goals. (OAG Canada, 2005). In fact, these concerns are not exclusive to the public sector, as it has been noted that private foundations could also face governance issues. (Gloria, M.J., 2022; OIG-USAID, 2020)

Performance audits conducted in Canada, the U.S. and the U.K. have shown that these concerns are real and well-founded. For instance, a recent audit of the Office of the Auditor General of Canada concluded that a foundation, Sustainable Development Technology Canada (SDTC), did not always manage funds in accordance with the terms and conditions of the contribution agreements and with its legislative mandate. The audit found that some funded projects were ineligible, conflicts of interests were poorly managed, and several legal requirements were not met. SDTC violated its conflict-of-interest policies 90 times, awarded $59 million to 10 projects that were not eligible and frequently overstated the environmental benefits of its projects. Soon after the report was tabled, the Minister announced that SDTC was abolished. (OAG Canada, 2024)

Based on these examples and the potential concerns rising from the inherent risks of these mechanisms, OAG Manitoba concluded that a performance audit of the use of trusts and funds, could be used to examine the potential ramifications of observations made through its financial audits.

The audit plan for this audit explored several lines of enquiries that could help elucidate the impact of trusts and funds on the quality and nature of the managements of public funds distributed in through these mechanisms. The audit focused on:

- Risk management considerations: As demonstrated by OAG Manitoba financial audits and performance audits conducted in other jurisdictions, several factors must be considered when determining the use of these funding mechanisms. It is important that they are carefully documented and analysed from a risk management perspective. They should also consider the magnitude and likelihood of these risks and any mitigations that should be undertaken.

- Guidance provided: The funds are transferred under the umbrella of an agreement. These agreements should include accountability expectations consistent with guidance from the provincial government for funding arrangements.

- Use of agreements with recipients: The government should monitor these agreements with recipients to ensure that objectives and expected outcomes were achieved.

- Availability and quality of accountability information: Finally, the information collected through the monitoring activities of the government should be accurate, reliable, and reported publicly. The absence of such information should also be reported and explained.

The audit work on this performance audit is still on-going and will be reported to the Legislative Assembly of Manitoba in 2025-2026.

Conclusion

Trusts and funds could be useful and are legitimate funding mechanisms for governments as they provide a certain level of flexibility and efficiency that could contribute to the achievement of policy objectives. However, they also raise some potential concerns with respect to control by the government and accountability for results achieved. In that respect, performance audits could be a fruitful extension of the financial audits. Financial statement audits are a great way of assessing accounting treatment of these arrangements but are not always able to dig deeper into “softer”, organizational issues that are mingling ethics, efficiency and governance challenges. Performance audits can extend and deepen the insights of financial audits and provide recommendations that could strengthen accountability and governance while providing useful lessons learned to ensure that future implementation of these funding agreements are robust and provide the accountability required to ensure that policy goals are achieved with integrity.

References

- Congressional Research Services. Universities and Indirect Costs for Federally

- Funded Research. 2025

- Glorya, M. J., Julia Kalmirah and Charlie Heatubun. 2022 “Funding for Sustainability: Three Challenges of Trust Fund Implementation in Papua, Indonesia” Preprints. https://doi.org/10.20944/preprints202209.0266.v1

- Government of the Province of Manitoba, Financial Administration Manual, 2025.

- Office of the Inspector General, U.S. Agency for International Development, Improved Guidance, Data and Metrics Would Help Optimize USAID’s Private Sector Engagement. 2020.

- Office of the Auditor General of Canada. Chapter 4: Accountability of Foundations. 2005

- Office of the Auditor General of Canada. Report 6: Sustainable Development Technology Canada. 2024.

- Office of the Auditor General of Manitoba. Public Accounts and Other Financial Statements. 2019.

- Office of the Auditor General of Manitoba. Public Accounts and Other Financial Statements. 2021.

- Office of the Auditor General of New Brunswick, New Brunswick Innovation Foundation. 2009.

- Office of the Auditor General of Nova Scotia, Effectiveness of the Green Fund Over First Two Years. 2023.

- Office of the Auditor General of Ontario. Chapter 4: Ontario Trillium Foundation. 2013

- Person, A.E. et al. Maximizing the Value of Philanthropic Efforts through Planned Partnerships between the U.S. Government and Private Foundations, Mathematica Policy Research Inc. 2009.

- U.K National Audit Office, Monitor : Regulating NHS foundation trusts. 2014.