Author: Laila Kikuste

Introduction

In response to public demand and global trends, the State Audit Office of Latvia (SAI of Latvia) has initiated the most significant transformation in its audit operations in the past two decades.

To improve efficiency and enhance the specialization of human resources, the financial audit function has been centralized within a single structural unit. Previously, financial audits were carried out across all audit departments. This shift reflects a strategic commitment to modernize audit practices, strengthen institutional capacity, and ensure greater consistency, quality and impact in the financial audit process.

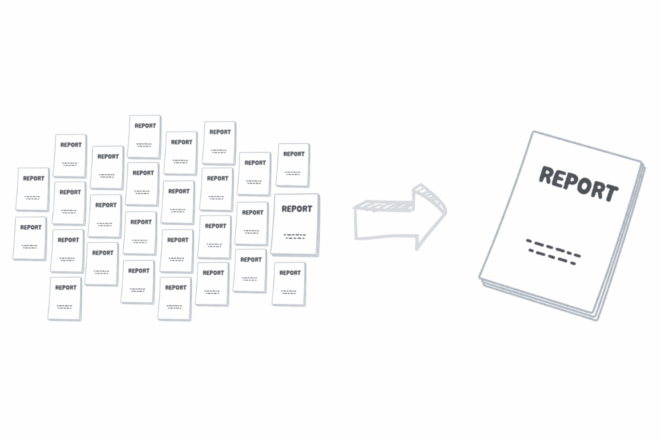

As a result, a single financial audit will be conducted and one audit report will be prepared, containing an opinion on the Consolidated Annual Financial Statements of the Republic of Latvia, which encompasses the annual reports of all state ministries, central government institutions, municipalities and derived public persons.

Background

Each year, in accordance with the State Audit Office Law and the Law on Budget and Financial Management, and within the statutory deadlines, the SAI of Latvia must conduct financial audits of the financial statements of ministries and central government institutions. Moreover, the SAI of Latvia must prepare and submit an audit report and an opinion on the State’s consolidated annual financial statement to the Parliament of Latvia.

What was the previous approach?

Each year, the SAI of Latvia engaged 13 audit sectors in conducting financial audits. The institution comprised six departments, further divided into 17 sectors, meaning that three-quarters of all sectors participated in financial audits. These audits were primarily conducted from the summer or autumn of one year until April of the following year. As a result, 27 financial audit reports were produced – 14 covering the annual financial statements of ministries, 12 covering the annual financial statements of central government institutions, and one addressing the State’s consolidated annual financial statement. In total, 27 audit reports and opinions were completed. In parallel with financial audit activities, the engaged sectors also conducted performance and compliance audits.

Why was the shift made?

The SAI of Latvia began considering changes to the financial audit process because the most recent financial audit results suggested that the quality of annual financial statements prepared by ministries and central government institutions had improved. For example, the number of unmodified opinions issued by the SAI of Latvia regarding the accuracy of annual financial statements had stabilized, as had the number of audit reports in which the SAI did not identify any deficiencies in their preparation. Each year over the past three years, only one or two cases out of 26 opinions revealed significant errors or scope limitations in the annual financial statements, where the exact amount of the error could not be determined. On average, in 63% of cases, auditors had not identified any issues requiring inclusion in an audit report (audit reports prepared without findings). These improvements resulted from cooperation among ministries, central government institutions and SAI of Latvia. Approximately 95% of errors identified by auditors are corrected or addressed during the financial audit process, and this practice is expected to continue.

Moreover, the State Treasury and State institutions have undertaken a series of actions over the past several years to implement many significant recommendations, such as: enhancing the regulatory framework by adopting a substantial part of the International Public Sector Accounting Standards (IPSAS), and improving the number of processes which are prerequisites for a well-organized internal control system and the proper preparation of annual financial statements. The Treasury is also implementing a project for the centralization of the accounting of state institutions.

The number of recommendations provided in financial audits has also been decreasing in recent years. In its assessments of the 2021 annual financial statement, SAI of Latvia issued 20 recommendations for improvement, and in 2022, provided 21 recommendations. This is a relatively small number compared to the period from 2016 to 2020, when 180 recommendations were issued over the entire period.

International experiences have also shown that centralizing the financial audit function within a single unit of the SAI can lead to positive outcomes, including improved consistency and efficiency.

The aforementioned facts determined the grounds for SAI of Latvia to review and optimize its approach to financial audits, aiming to achieve the correctness of the annual financial statements with a lower resource input, thereby redirecting the saved resources towards performance audits.

How were the changes carried out?

Formally, the entire process lasted from June 2022 to May 2025; however, on the practical level the process started much earlier with feasibility studies, discussions and estimates.

During the period from June 2022 to May 2025, it was necessary to amend the State Audit Office Law, followed by corresponding adjustments to internal regulatory acts. Overall, it was necessary to:

- Change the audit approach, which included revising the materiality and assurance levels, as well as changing the way the audit scope is determined;

- Optimize the audit process itself, which involved centralizing as many audit steps and procedures as possible, standardizing audit programs;

- Implement structural changes, including staff rotation and specialisation.

As part of the audit process optimization, substantial efforts were dedicated to the standardization of audit programs and the development of automated data analysis solutions. Multiple internal working groups composed of SAI of Latvia auditors were formed, culminating in the development of eight standardized audit programs and seven automated data analysis tools. Three audit tools were also purchased from an external programme developer. This represents an important step towards ensuring that the team operate according to a unified approach and handles a larger volume of data.

The structural reform of the SAI was equally important, whereby the previous structure of 13 sectors involved in financial audits was consolidated into a single department comprising three sectors, functioning as one unified financial audit group. While previously 93 employees, including auditors and management), were involved in financial audits, either partially or fully, and at various levels, including at the management level, currently 31 employees are involved full-time, including four in management roles.

Lessons learnt

Financial audits will be conducted by a single department, consisting of three sectors, and will operate as one unified audit group. Upon completion of the audit, a single report will be prepared, which will also include the opinion. We have learned that:

- Time Matters. Significant changes in organizational structure and processes require time to implement effectively, as they involve not only procedural adjustments, but also shifts in mindset, roles and collaboration practices across the organization. Moreover, these changes affect and require the alignment of external stakeholders, including the need for legislative amendments – a process that is inherently time-consuming.

- Employees Matter. It is crucial to communicate with employees openly and provide thorough explanations about upcoming changes to prevent uncertainty and misunderstandings. By addressing concerns and fostering a transparent dialogue, we can ensure that everyone is on the same page, in order to ultimately reduce the number of qualified personnel which may leave the institution under uncertainty. Equally important was the active involvement of staff in the practical aspects of the transformation. Their participation in activities, such as the standardization of audit programs, enabled employees to better understand and accept the purpose of the changes, and to recognize the benefits these changes would bring. Experienced employees are our greatest asset, and their knowledge and expertise will play a key role in successfully navigating this transformation.

- Resources Matter. By implementing changes, we can allocate more resources to performance and compliance audits and use financial audit resources more efficiently.

- Innovation Matters. The standardization of audit programs and the development of automated data analysis solutions is a significant step forward in enhancing efficiency and accuracy. It ensures that larger volumes can be audited more effectively while maintaining consistency, allowing all teams to work according to a unified approach. This modernization not only streamlines the process but also strengthens the overall quality of the audits.

We embarked on this challenging transformation as we began a new chapter on 1 May 1, 2025. What remains certain, however, is our strong commitment to progress and to delivering greater value through our work for the benefit of society.