An “Ecological Transition Community” fuels the French Cour des Comptes with Tools

By Éric Allain, Senior auditor, President of the Energy Division, and Sandrine Crouzet, Regional Audit Chamber First Advisor.

Considering the rise in environmental concerns and the growing importance of ecological transition issues in all national and local public policies, the French Cour des comptes, the supreme audit institution (SAI) that forms the financial jurisdictions with the regional and territorial audit chambers (CRTCs), has organized with the latter to strengthen the relevance of their audit and assessment work in these areas, which already account for a growing share of their scheduled work.

While the aim is to step up the pressure of audits on these subjects, which represent growing public financial stakes (in terms of budget spending, taxation, but also “ecological debt”), it is also necessary to strengthen auditors’ capabilities on these complex, sometimes controversial subjects. An original approach has been taken, in the form of an “Ecological Transition Community” (ETC).

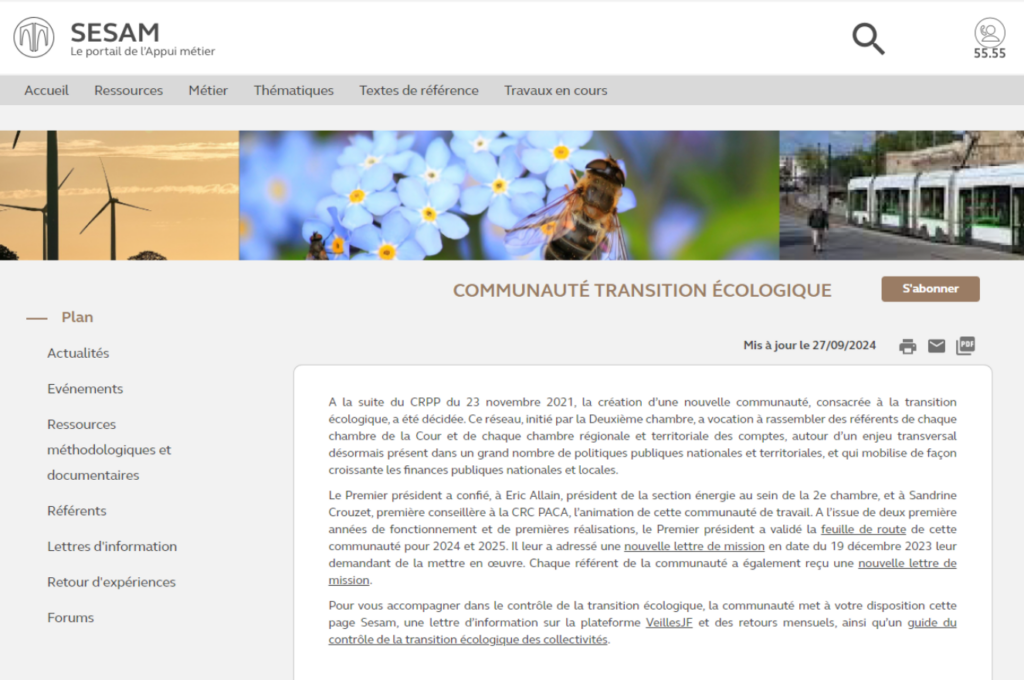

The ecological transition community has a portal on the financial jurisdictions’ intranet. Source: French Cour des comptes

The financial jurisdictions’ ecological transition community was created in February 2021 with the aim of promoting and fostering ecological transition control, whether at the level of the French Court’s chambers or CRTCs.

The community is made up of two co-leaders, one a magistrate at the Court and the other at the CRTC, and referents (or representative) within each chamber (Court and CRTC), the General Prosecutor’s Office and each of the Court’s support departments.

Meeting on a monthly basis and also divided into working groups, the ecological transition community provides all control teams with tools to help them better master the challenges of ecological transition and include this cross-functional dimension in their controls:

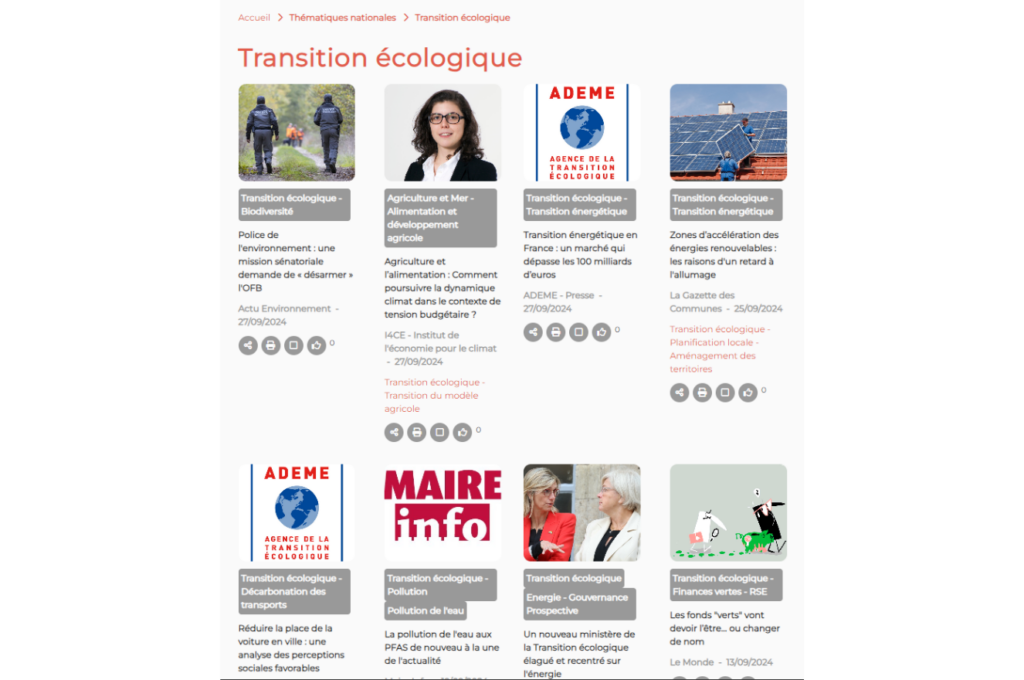

- A monthly newsletter, with articles on the ecological transition, global warming, decarbonization of several sectors (energy, agriculture, transport) and regional planning for the transition;

- Feedback from audits in the form of meetings/video conferences/other events held at the Court or at CRC on an area of ecological transition. This monthly feedback is open to all;

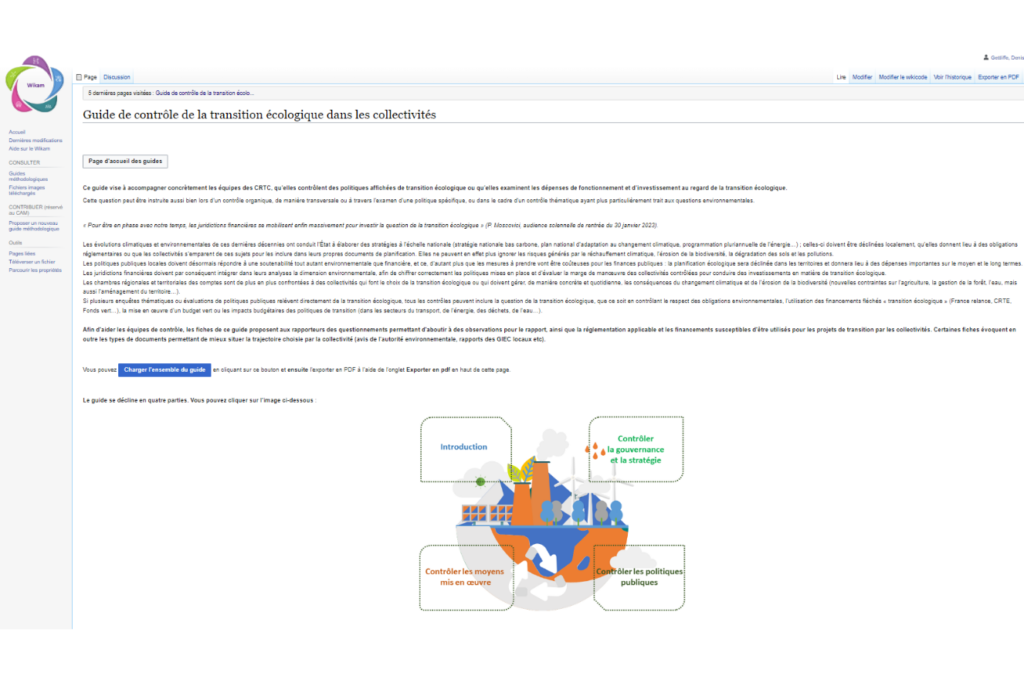

- A guide in “wiki” format that is collaborative, for auditing the ecological transition of local authorities. Each of the guide’s sheets sets out the issues at stake in the topic covered, recalls the regulatory obligations for carrying out a regularity audit, and proposes a questionnaire that can be reused by audit teams. The guide also presents a methodology for integrating the transition audit into all the aspects usually present in an audit of accounts and management (financial analysis, human resources, budget steering, assets). The guide has been available to audit teams since November 2023.

- Conferences or webinars, two or three times a year, during which external speakers present financing mechanisms for the ecological transition, think-tank reports on the subject, evaluation mechanisms, etc.

- Training, in conjunction with the job-support center, either on the ecological transition itself or on sectoral ecological transition control methods

- A documentation area for easy access to all these tools.

The ETC works continuously to improve existing tools: the format chosen for the control guide allows for the addition of sheets, links with other thematic control guides including sections on the ecological transition, and regular updating of regulatory references. A working group, made up of referents and non-referents, drafts and reviews the sheets on a collegial basis.

The more recent creation of two other working groups is increasing the community’s thinking on transition control:

- an “international” working group, with the participation of the Court’s international department, will identify the methodologies and best practices applied in other supreme audit institutions, interview foreign experts and strengthen the participation of French financial jurisdictions within INTOSAI and other international institutions gathering SAIs, as well as in existing partnerships;

- a think-tank on environmental accounting and green budgets has also been set up, with the aim of looking into control methods that are still little-known today(1) and joining in current discussions on how to take account of the ecological transition in accounting.

Since the creation of the community, the number of referents per chamber has increased (up to three referents appointed by the Chairman of the Chamber). Some CRTCs have also set up internal ecological transition centers. Their role is to propose audits on this theme in their chamber’s programming, to support colleagues wishing to introduce an ecological transition component into their audits, and to set up in-house training programs to enhance agents’ skills.

The work carried out over the past two years by the ecological transition community, now well identified within the financial jurisdictions, will serve as a basis to facilitate everyone’s work with a view to the annual report on ecological transition, announced by the First President of the Cour des comptes and scheduled for publication in September 2025. This prospect encourages the community to refine its tools and promote local training through referents.

The increase in the number of referents, as well as in the number of participants in the monthly feedback sessions, demonstrates the growing interest of our colleagues in these issues. In this sense, the community has achieved part of its objectives: it has demonstrated that transition control is not the exclusive domain of certain control teams, but can, and indeed should, be practiced by all; it has strengthened the capacity for action of financial jurisdictions in this field.

These efforts must be maintained to ensure that the ecological transition becomes as systematic an area of control as human resources, financial analysis, gender equality or real estate policy. The next step will be to make the ecological transition not just an area of control, but a cross-cutting issue in all aspects of financial and management controls, and in all public policy evaluations.