Building Partnerships to Combat Fraud, Corruption Via Effective SAI Technical Support

[cmsmasters_row data_width=”boxed” data_padding_left=”3″ data_padding_right=”3″ data_top_style=”default” data_bot_style=”default” data_color=”default” data_bg_position=”top center” data_bg_repeat=”no-repeat” data_bg_attachment=”scroll” data_bg_size=”cover” data_bg_parallax_ratio=”0.5″ data_padding_top=”0″ data_padding_bottom=”50″ data_padding_top_laptop=”0″ data_padding_bottom_laptop=”0″ data_padding_top_tablet=”0″ data_padding_bottom_tablet=”0″ data_padding_top_mobile_h=”0″ data_padding_bottom_mobile_h=”0″ data_padding_top_mobile_v=”0″ data_padding_bottom_mobile_v=”0″ data_shortcode_id=”uwjnc61m2″][cmsmasters_column data_width=”1/2″ data_bg_position=”top center” data_bg_repeat=”no-repeat” data_bg_attachment=”scroll” data_bg_size=”cover” data_border_style=”default” data_animation_delay=”0″ data_shortcode_id=”mfm79s1j97″][cmsmasters_image shortcode_id=”yit3fprn2o” align=”center” link=”http://intosaijournal.org/wp-content/uploads/2019/04/INTOSAI-Journal-Spring-2019_40.jpg” animation_delay=”0″]19063|http://intosaijournal.org/wp-content/uploads/2019/04/INTOSAI-Journal-Spring-2019_40-580×751.jpg|cmsmasters-project-masonry-thumb[/cmsmasters_image][/cmsmasters_column][cmsmasters_column data_width=”1/2″ data_shortcode_id=”1fzxdpmf4q”][cmsmasters_image shortcode_id=”jrz40tju3″ align=”center” link=”http://intosaijournal.org/wp-content/uploads/2019/04/INTOSAI-Journal-Spring-2019_41.jpg” animation_delay=”0″]19064|http://intosaijournal.org/wp-content/uploads/2019/04/INTOSAI-Journal-Spring-2019_41-580×751.jpg|cmsmasters-project-masonry-thumb[/cmsmasters_image][/cmsmasters_column][/cmsmasters_row][cmsmasters_row data_shortcode_id=”rnhq3foblq” data_width=”boxed” data_padding_left=”3″ data_padding_right=”3″ data_top_style=”default” data_bot_style=”default” data_color=”default” data_bg_position=”top center” data_bg_repeat=”no-repeat” data_bg_attachment=”scroll” data_bg_size=”cover” data_bg_parallax_ratio=”0.5″ data_padding_top=”0″ data_padding_bottom=”50″ data_padding_top_laptop=”0″ data_padding_bottom_laptop=”0″ data_padding_top_tablet=”0″ data_padding_bottom_tablet=”0″ data_padding_top_mobile_h=”0″ data_padding_bottom_mobile_h=”0″ data_padding_top_mobile_v=”0″ data_padding_bottom_mobile_v=”0″][cmsmasters_column data_width=”1/1″ data_shortcode_id=”docs6t3tbb” data_bg_position=”top center” data_bg_repeat=”no-repeat” data_bg_attachment=”scroll” data_bg_size=”cover” data_border_style=”default” data_animation_delay=”0″][cmsmasters_notice shortcode_id=”x0hpmadv8r” type=”cmsmasters_notice_success” animation_delay=”0″]

Click here to download full article

[/cmsmasters_notice][/cmsmasters_column][/cmsmasters_row][cmsmasters_row][cmsmasters_column data_width=”1/1″][cmsmasters_text]

by Wilf Henderson, International Technical Cooperation Project Manager (Retired), United Kingdom National Audit Office

Preventing fraud and corruption are major challenges facing governments, particularly those of developing countries. Government inability to establish effective internal audit and financial control systems and adequately establish or resource organizations charged with identifying fraud and corruption are just some causes of fraudulent and corrupt behavior.

While no system exists to entirely avert fraud and corruption, there are measures that can be implemented to reduce the potential of occurrence.

Supreme Audit Institutions (SAIs) provide assurance that public monies have been properly accounted for and are in keeping with established laws and regulations. While not the SAI’s responsibility to investigate and uncover evidence of fraudulent and corrupt behavior, a general expectation exists (stemming from society and the media) that SAIs have a major responsibility in its prevention. SAIs in developing countries often face considerable challenges and may lack the capacity to undertake effective audits and seeking support from development partners to enable technical assistance is a crucial component to improving audit quality.

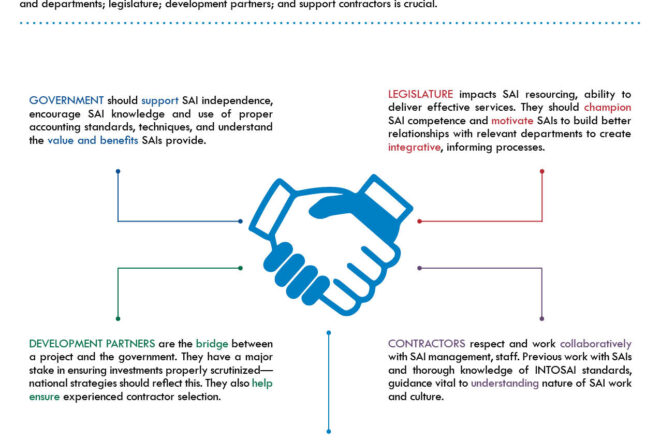

To thwart fraud and corruption, building and maintaining relationships with government, its ministries, departments and agencies; legislature; development partners; and support contractors is crucial. SAIs should also cultivate connections, where applicable, with the Public Accounts Committee (PAC) anti-corruption bodies, and judiciary and prosecuting authorities, as reporting and following up on cases of fraud and corruption, when necessary, are important steps.

These relationships must be based on trust and mutual respect. Each stakeholder must be clear on the roles and responsibilities necessary to minimize fraud and corruption, and in my experience in providing technical support to developing SAIs in Sub Saharan Africa, there are key actions required.

Government

- Government should be fully supportive of an independent, competent SAI. Encouraging knowledge and use of proper accounting standards and techniques is essential while also understanding management must implement systems and procedures to detect and prevent fraud and corruption.

- Government must understand the value of SAIs. Effective audit work promotes good governance and leads to improvements in internal financial control systems.

- Government should establish effective internal financial control systems, adequately fund bodies charged with combating and prosecuting cases of fraud and corruption and sufficiently resource internal audit.

Legislature

- Legislature should ensure SAIs are resourced to deliver effective, objective public audits.

- Legislature should champion a competent SAI to build better relationships and processes with relevant prosecuting authorities and the PAC. Strengthened relations creates integrative, informing processes with each organization fully understanding roles and responsibilities.

Development Partners

- Development Partners (DPs) bridge technical assistance projects and government and are often substantial investors having a major stake in ensuring investments are properly scrutinized. This need should be recognized within national strategies, and SAI development should be included in any major public reform program.

- DPs are important to ensuring requested technical assistance project support providers are competent, experienced contractors with comprehensive knowledge of SAI work.

SAI Management

- Leadership is essential to a project’s efficient functioning and set the tone throughout the SAI and with support providers. Employing a collaborative approach is key to projects thriving in an inclusive and supportive environment.

- Work plans should not encourage auditors to seek out fraud and corruption but to inform appropriate authorities if suspicious activities are uncovered. SAI management should ensure follow-up action on such cases has been taken.

- Leaders should ensure organizational buy-in, particularly given the potential changes to a change-averse culture. Establishing an inclusive learning environment incorporating staff at all levels is one method to achieve consensus.

Contractors

- Successful contractors respect and work alongside SAI management and staff collaboratively and recognize potential challenges within the working environment with an ability to empathize with staff facing change.

- Consultants should have experience with SAI work, thorough knowledge of International Organization of Supreme Audit Institutions (INTOSAI) standards and understand SAI roles and responsibilities in combating fraud and corruption.

[/cmsmasters_text][/cmsmasters_column][cmsmasters_column data_width=”1/1″ data_shortcode_id=”61cje0ksxc” data_bg_position=”top center” data_bg_repeat=”no-repeat” data_bg_attachment=”scroll” data_bg_size=”cover” data_border_style=”default” data_animation_delay=”0″][/cmsmasters_column][/cmsmasters_row]