Applying Strategic Foresight in Performance Audit: Case Study of Audit of Energy Transition in Indonesia

Authors: Pemut Aryo Wibowo, Normas Andi Ahmad, Audit Board of the Republic of Indonesia

Abstract

Future uncertainty, driven by factors such as climate change, technological advancements, and global dynamics, poses challenges that require organizations and governments to adopt more flexible, adaptive, and resilient approaches to planning. SAIs play a crucial role in addressing climate change and future uncertainty by providing insights into the effectiveness of climate-related initiatives and fostering greater accountability and transparency. Strategic foresight in auditing is essential for anticipating and preparing for future uncertainties, enabling organizations to navigate risks and opportunities proactively. Applying a six-step foresight framework in auditing the energy transition, particularly in the electricity sector, allows auditors to evaluate progress, identify gaps, and provide recommendations for more sustainable and resilient energy policies. By integrating strategic foresight into auditing practices, organizations can better prepare for the complexities of a rapidly changing world and build resilience against future uncertainties.

I. Role of SAIs in Addressing Climate Change and Future Uncertainty

Climate change is one of the factors that exemplifies a powerful force driving future uncertainty. The unpredictability of climate-related events, such as extreme weather, rising sea levels, and shifting ecosystems, introduces a level of uncertainty that challenges traditional models of planning and decision-making. As these factors interact with other global challenges like geopolitical tensions and technological advancements, the future becomes increasingly difficult to predict, making it essential for organizations and governments to adopt more flexible and adaptive approaches to planning.

Supreme Audit Institutions (SAIs) play a pivotal role in addressing the challenges posed by climate change and future uncertainty. As independent entities tasked with evaluating government policies and expenditures, SAIs are uniquely positioned to assess the effectiveness of climate-related initiatives and ensure that public resources are being used efficiently and effectively (INTOSAI, 2019). In the face of growing uncertainty, SAIs can provide critical insights into how well governments are preparing for the impacts of climate change, from mitigation efforts to adaptation strategies. SAIs can also foster greater accountability and transparency in how governments address climate change and manage uncertainty. Through rigorous audits, they can hold governments accountable for their commitments to climate action, ensuring that targets are met and resources are not misallocated.

The Audit Board of the Republic of Indonesia (BPK), as the nation’s supreme audit institution, plays a vital role in promoting effective climate governance and management. In a country as diverse and dynamic as Indonesia, addressing climate change while maintaining a balance between economic growth, social progress, and environmental sustainability is a significant challenge. BPK actively engages in this complex task by ensuring that climate-related policies and actions are both effective and aligned with the principles of sustainable development. By conducting thorough audits of climate initiatives and policies, BPK provides a crucial oversight function that helps to ensure that Indonesia’s approach to climate change is both robust and equitable.

As organizations face complex challenges such as technological disruption, climate change, and shifting geopolitical landscapes, there is a growing need for audits that not only assess the present but also anticipate the future (Butaka, 2022). This is where strategic foresight becomes invaluable, offering a proactive approach to auditing that enables organizations to navigate uncertainties and align their strategies with potential future scenarios. By integrating foresight into the audit process, auditors can identify emerging risks, trends, and opportunities that may impact the organization in the long term (Hay, 2019). This proactive approach helps auditors to not only assess current performance but also to evaluate how well an organization is positioned to adapt to future challenges.

II. Strategic Foresight in Auditing

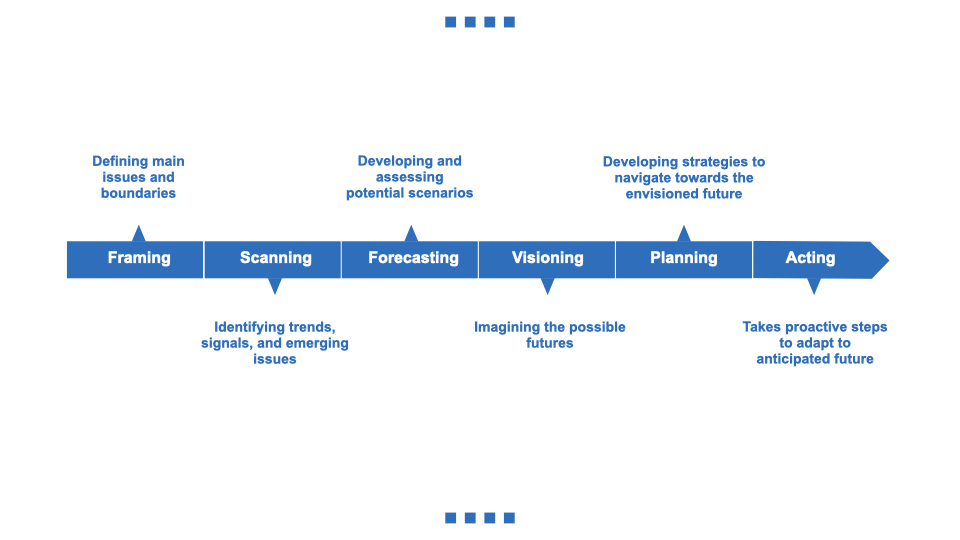

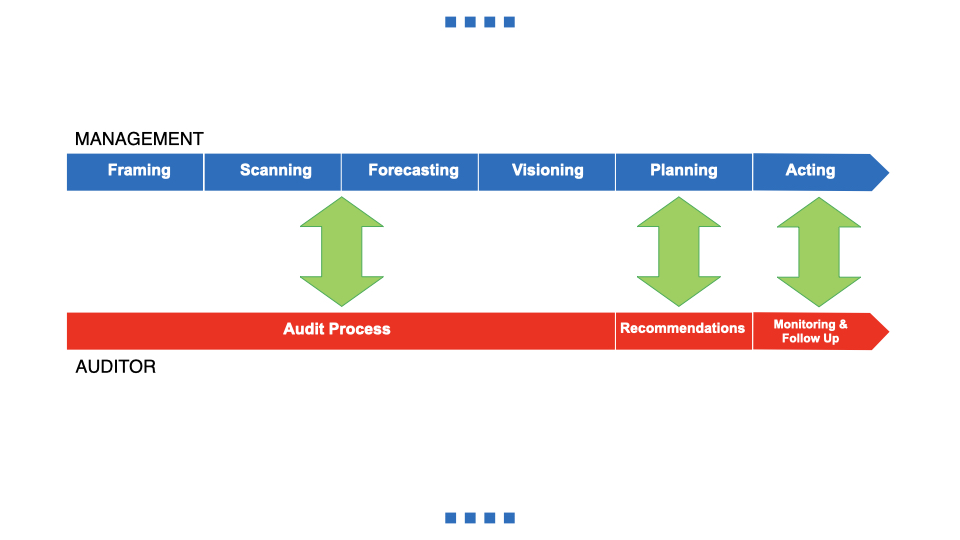

One of the strategic foresight frameworks is the six-step foresight framework developed by Hines and Bishop (2007). This framework is compatible with auditing process as it offers enhanced decision-making by providing insights into the long-term implications of different scenarios on targets achievement and organizational operations, thereby ensuring that the organization remains resilient and adaptable over time (Kramer, 2023). The process begins with framing, where the main issues and scope, considering the broader context of the government’s strategic goals and the uncertainties it faces, are defined. This step sets the stage for scanning, which involves gathering information from various sources to identify trends, signals, and emerging issues that could impact the government or institutions. Scanning process helps auditors to build a comprehensive understanding of potential future developments, enabling them to identify relevant risks and opportunities that may not be apparent through traditional auditing methods. It provides a more organized perspective on the major trends and shifts happening in an organization’s environment, helping to inform policy decisions (Habegger, 2010).

The next steps, forecasting and visioning, involve developing potential scenarios based on the information gathered and imagining the possible futures. Moreover, forecasting can be used to assess the scenarios to predict how different variables might affect the achievement of the strategic goals (FasterCapital, 2024). Visioning, on the other hand, helps auditors and stakeholders to articulate a desired future state, considering the best-case scenarios. Planning then involves developing strategies to navigate towards the envisioned future, including risk mitigation and resource allocation. Finally, acting is the implementation phase, where the government and institutions takes proactive steps to adapt to anticipated changes. By integrating this foresight framework, auditors can move beyond retrospective analysis, providing valuable insights that help organizations to be resilient and adaptive in the face of uncertainty.

III. Applying Strategic Foresight in the Audit of Energy Transition

Energy sector is the largest contributors to global greenhouse gas emissions, making it a focal point in the fight against climate change (Climate Watch, 2024). Energy transition is a critical pathway to mitigating climate change, representing a shift from fossil fuel-based energy systems to more sustainable, renewable sources. In Indonesia, the energy sector accounted for 59.19 percent of the country’s greenhouse gas emissions in 2022, with power generation contributing 40.7 percent of the emissions within the energy sector (Ministry of Environment and Forestry, 2024).

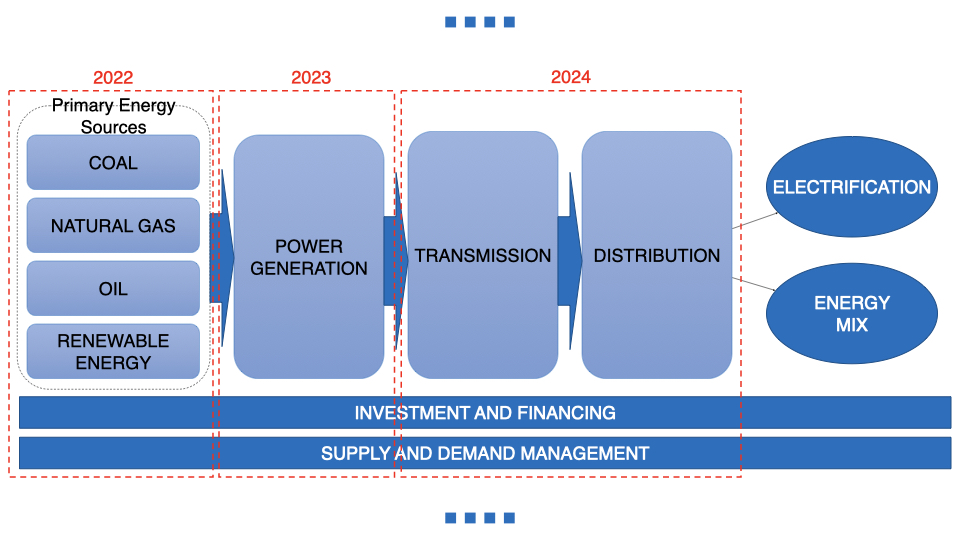

The implementation of strategic foresight framework in performance audit is piloted in the audit of energy transition, especially in power generation. The foresight process will involve a series of audits starting from 2022 to 2024 and the comprehensive foresight on energy transition is expected to be issued in 2025. In the first year, the audit concentrated on the management of energy sources, including coal, natural gas, and renewable energy, to assess how well these resources are being utilized and managed. The second year focused on power generation and the final year will be focused on transmission and distribution.

In the framing stage, the main objective and scope of energy development are defined. They include key stakeholders, potential risks, and the specific aspects that need scrutiny, such as policy implementation, infrastructure development, or financial investments. The balance among the three aspects of the energy trilemma—energy security, energy affordability, and environmental sustainability—is also considered as one of the main issues. The process is then followed by scanning, where influential data are gathered from various sources, which include technological trends, geopolitical risks, regulatory changes, and environmental impacts. This comprehensive information gathering helps in identifying emerging issues, opportunities, and challenges that could influence the energy transition. In the forecasting phase, auditors analyze the gathered data to assess potential future scenarios, considering different paths the energy transition might take. These scenarios are then used in the visioning stage to outline desirable future states, helping to set long-term goals that align with energy transition objectives and national energy policies.

The audit result is expected to positively influence the actionable strategies to achieve the envisioned outcomes, incorporating risk management and resource allocation in the planning stage. Finally, in the acting stage, auditors monitor the implementation of these strategies and recommendations, providing feedback and making adjustments as needed to ensure that the energy transition progresses smoothly and effectively, while also meeting regulatory and sustainability targets. The final results of the series of audit will then be compiled into a comprehensive report that provide a strategic foresight of Indonesia’s energy transition to address climate change.

IV. Results and Analysis

For the first year, the audit produced forward-looking and future-oriented results that emphasize the need for strategic adjustments to current energy policies (BPK, 2023). The audit revealed that while there has been notable progress in adopting sustainable energy system, existing infrastructure and regulatory frameworks may struggle to accommodate the rapid changes expected in the near future. The potential gaps and rooms for improvement that highlighted in the audit include:

- Potential increase in energy subsidies that needs to be mitigated due to the anticipated shift towards renewable energy, which is likely to elevate electricity production costs. Given that the electricity sector in Indonesia is still subsidized by the Government and assuming there will be no tariff increases in the near future, this rise in production costs would significantly impact the subsidy amount required. Without adjustments to tariffs, the Government would need to allocate more resources to cover the higher generation costs, thereby increasing the financial burden of subsidies.

- Despite several commitments made toward financing the energy transition in Indonesia, there remains a significant gap in identifying and mobilizing the necessary funding schemes and sources for key projects. The Government has yet to specify how it will finance the early retirement of coal power plants, a critical step in the transition process. Furthermore, a comprehensive analysis of the energy transition’s impact on state finances has not been undertaken. This lack of clarity and planning around funding and financial impacts poses challenges to the successful implementation of Indonesia’s energy transition goals, potentially hindering progress and long-term sustainability.

- Early coal retirement initiative lacks a thorough cost and benefit analysis, which is crucial for evaluating its long-term viability and impact. The initiative has not adequately considered alternative energy sources, including their reliability and affordability, which are essential for ensuring a stable energy supply post-transition. Additionally, the potential issue of stranded assets resulting from the retirement of coal power plants has not been fully addressed. Without these critical evaluations, the initiative risks creating economic and energy security concerns that could undermine its intended benefits.

- According to the Net Zero Emission roadmap, a significant portion of future economic activities in Indonesia is expected to be powered by solar panels. However, a critical dependency on foreign imports is identified, with about 70 to 80 percent of solar power plant components still being sourced from other countries. This reliance highlights a significant gap in the domestic industrial capacity, as local industries are not yet prepared to produce the necessary components to support the large-scale development of renewable energy in Indonesia. The lack of domestic production capabilities not only raises concerns about supply chain vulnerabilities but also limits the potential economic benefits of the energy transition, such as job creation and technological advancement within the country.

- The progress of electricity infrastructure development has been delayed, raising concerns about the stability and reliability of the electrical system in several regions. The predictive analysis indicates that if this slow pace of development continues and is not effectively mitigated, it could severely impact the security of the electrical grid. Insufficient infrastructure development could lead to power shortages, disruptions, and an inability to meet rising energy demands, especially as the country transitions to renewable energy sources.

The audit contributed valuable insights that help define the main issues and scope of the energy transition and identify key issues and information that need to be considered. By leveraging data and findings from audits, the process is better equipped to pinpoint emerging risks, opportunities, and trends. The audit results also play a crucial role by offering data-driven analyses that aid in predicting future challenges and opportunities. Ultimately, the outcomes of BPK’s audits inform the development and implementation of strategies, ensuring that they are aligned with the strategic goals and sustainability principles.

V. Conclusion and Way Forward

The pilot audit demonstrated that integrating the six-step strategic foresight framework into the auditing process significantly enhances decision-making capabilities. This approach not only offers valuable insights into the long-term implications of various scenarios on target achievement and organizational operations but also strengthens the organization’s ability to remain resilient and adaptable over time. By aligning audit outcomes with forward-looking perspectives, organizations can better anticipate and prepare for future challenges, thereby improving the overall effectiveness of their strategic planning and execution.

Given the success of the pilot audit, the subsequent audits are expected to assess other critical aspects as well as to monitor the implementation of recommendations of previous audit. The use of this approach is expected to provide a more robust and comprehensive foundation for understanding the complexities and future impacts of energy transition on strategic state goals. Following the completion of these series of audits, a comprehensive foresight report will be compiled and launched, offering an in-depth analysis of the findings and their implications. This report is expected to serve as a critical resource for guiding future decisions and strategies, ensuring that the organization is well-positioned to navigate the evolving energy landscape. By synthesizing the insights from the audits, the report will offer actionable recommendations that align with emerging trends, helping the government to proactively address challenges and seize opportunities in the dynamic energy sector.

About the Authors

Mr. Pemut Aryo Wibowo

Mr. Wibowo holds a master degree in accounting from Gajah Mada University. He is currently the Director of Audit in the Audit Board of the Republic of Indonesia who is responsible for overseeing audits on energy, environment, and natural resources management.

Mr. Normas Andi Ahmad

Mr. Ahmad is a senior auditor who has a Masters degree in Environment and Sustainable Development from Glasgow University. He is experienced in leading teams of audit on energy and natural resources management, as well as SDGs related audits.