Scanning Supreme Audit Institutions Independence: A Spotlight on Indirect Interference

Authors: Nicolás Lagos, PhD Candidate, Rutgers University, Osvaldo Rudloff, Lawyer, MSc y International Consultant

Introduction: The Importance of SAI Independence

The principle of independence is the cornerstone of credible public sector auditing. Foundational documents, as the Lima Declaration (INTOSAI 1977) the Mexico Declaration (INTOSAI 2007), and landmark United Nations General Assembly resolutions, including A/RES/66/209 (2011), A/RES/69/228 (2014), and the political declaration from the special session against corruption, A/S-32/L.1 (2021), support a global consensus that strong, independent SAIs are essential pillars of democratic accountability and public trust.

The imperative for robust independence is intensified by the evolving role of SAIs in modern governance. Driven by public management reforms (Bouckaert and Put 2016), SAIs have moved beyond their traditional focus on financial integrity to become key players in assessing the economy, efficiency and effectiveness of government programs (Pollitt and Summa 1997) (Power 2009). These organisations have adopted crucial governance and policy analysis functions, tackling complex and politically sensitive issues such as anti-corruption efforts (Dye and Stapenhurst 1998), environmental protection (OISC/CPLP 2023), and gender equality (OLACEFS 2019). As SAIs transition from being traditional watchdogs to influential partners in governance, their insulation from political and administrative pressure becomes more critical than ever. This evolution creates a fundamental tension between maintaining autonomy and having a direct impact on policy, requiring SAIs to carefully manage their relationships with stakeholders to ensure their findings remain impartial and credible (Pierre and De Fine Licht 2017).

While the independence principle is widely recognised, evaluating its implementation across SAIs remains challenging. This article analyses key global data to highlight lessons and best practices for strengthening independence throughout the INTOSAI community.

Our Data-Driven Framework for Analysis: IDI Global Stocktaking Report

Our analysis is based on data from the INTOSAI Development Initiative (IDI) Global Stocktaking Report (INTOSAI Development Initiative, 2024) which provides a comprehensive global assessment of SAIs performance and capacities.

However, in using this data, it is essential to acknowledge its strengths and limitations. The report’s primary value lies in its comprehensive scope and standardised data collection, which enable unprecedented global and regional comparisons. This allows the SAI community to identify systemic trends, shared challenges, and areas of collective strength. Conversely, a limitation is the report’s reliance on SAIs’ self-reported data. As academic studies have noted, a critical distinction exists between de jure institutional frameworks and the more nuanced de facto realities of day-to-day operations (Blume and Voigt 2011). Therefore, this article uses the report not as a definitive judgment on any single SAI, but as an indicator that illuminates the overall landscape of independence and guides the collective discussion and capacity-building efforts.

Key Insights from the 2023 IDI Global Stocktaking Report

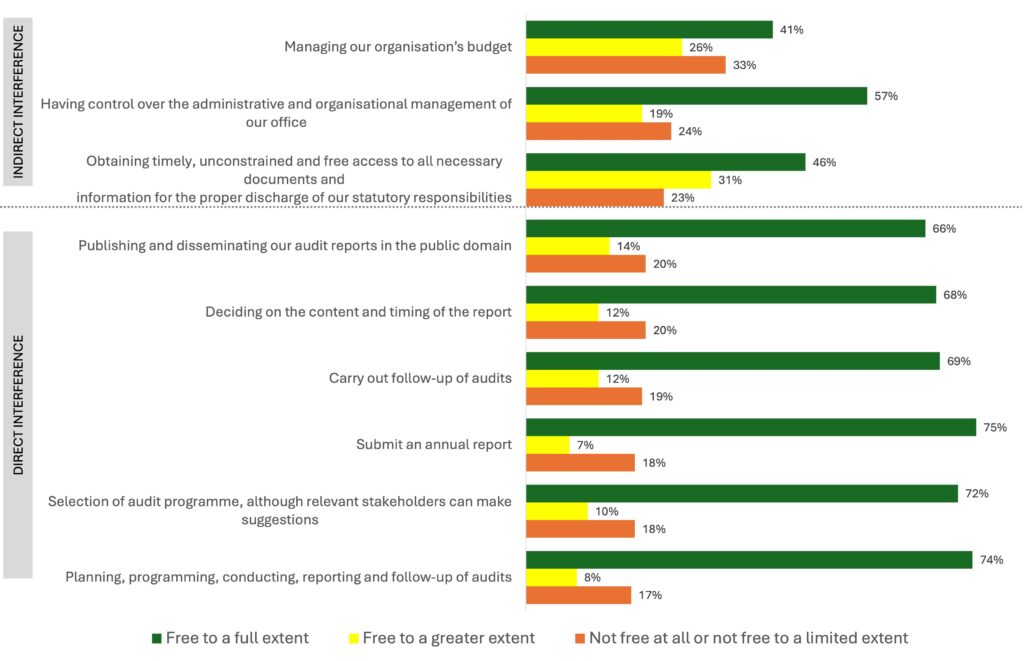

The Stocktaking Report offers the most comprehensive assessment of SAI performance worldwide. Of particular interest is Question 13, answered by 166 SAIs, which asked to what extent they were free from Legislative or Executive interference in core activities during 2020–2022. This approach moves the debate from abstract legal principles toward concrete situations where independence is undermined, making it possible to see how interference affects SAIs in practice.

The question distinguishes nine core activities in which SAIs may experience interference, which can be analytically grouped into direct and indirect forms. Direct interference refers to overt restrictions that strike at the heart of a SAI’s mandate and public accountability role and includes constraints on the selection of audit programmes, planning and conducting audits, submitting an annual report, deciding on the content and timing of reports, publishing audit reports in the public domain, and carrying out follow-up audits. In contrast, indirect interference captures pressures that do not formally alter the audit mandate but nonetheless erode the SAI’s autonomy to perform effectively. These interferences are reflected in limitations on obtaining timely and unconstrained access to documents and information, restrictions on managing the organisation’s budget, and reduced control over administrative and organisational management. This distinction underscores that independence can be undermined not only through visible encroachments on audit functions, but also through subtler operational constraints that quietly weaken the institution’s capacity to act.

The survey question employed a four-point ordinal scale ranging from “Not at all” (1), “To a limited extent” (2), “To a greater extent” (3), and “To a full extent” (4). For analytical purposes, the first two categories (Not free at all and Free to a limited extent) were combined. Both responses reflect the existence of interference – whether complete or partial – so grouping them provides a clearer picture of where SAIs encounter limitations in practice. In contrast, the last two categories (Free to a greater extent and Free to a full extent) capture situations in which interference was less present, making it possible to distinguish more easily between those activities where challenges are frequent and those where they are relatively rare.

The results show a consistent pattern across the nine activities. At the upper end, the vast majority of SAIs reported being free from interference when carrying out core audit tasks, including submitting an annual report (75%), planning and conducting audits (74%), selection of the audit programme (72%), and follow-up of audits (69%). Similarly, over two-thirds indicated no interference in deciding on the content and timing of reports (68%) and publishing audit findings (66%). By contrast, the lowest levels of freedom from interference are observed in indirect dimensions. Only 41% of SAIs reported being fully free from interference in budget management, 46% in obtaining timely access to documents and information, and 57% in administrative and organisational management. These findings highlight a clear distinction: while most SAIs can perform their formal audit functions without significant obstruction, a considerable proportion still face constraints in the internal and operational conditions necessary to sustain those functions effectively.

Image 1: Extent of Reported Freedom from Interference in SAI Activities (2020–2022)

Why it is Important to Focus on Indirect Interference

For decades, both academic debates and practitioner reforms have framed SAI independence as a fundamental pillar for effective public auditing. Much of this attention has concentrated on high-level political independence – protecting SAIs from overt political pressures, undue interventions to avoid scrutiny, restrictions on the audit mandate, or limitations on the dissemination of reports. While such forms of direct interference remain relevant, the data show that they are not the only, nor necessarily the most frequent, threats that SAIs face in practice.

The evidence highlights that indirect interference is increasingly shaping the daily functioning of SAIs. This interference manifests in two main ways. First, there are constraints on internal management, particularly regarding financial, human, and technological resources. Limiting the control that SAIs have over their budgets restricts their ability to plan and invest in the medium and long term, resulting in insufficient staffing, difficulties in retaining qualified personnel, and inadequate access to modern technologies required for complex audits. These constraints weaken institutional capacity from within, gradually undermining effectiveness even when formal independence is guaranteed by law.

Second, there are barriers to timely and unrestricted access to information, which is indispensable for fulfilling statutory responsibilities. Even if legal frameworks formally grant broad mandates, SAIs cannot perform their work if audited entities delay, obstruct, or provide incomplete data. This undermines the quality of audit findings and diminishes their relevance for accountability and policymaking. In practice, audit teams face these obstacles daily, often with more immediate impact than high-level political interference.

Therefore, while it remains essential to continue strengthening the legal and constitutional safeguards of SAI independence, it is equally important to focus on the operational realities that audit institutions face. Paying attention to how senior management and audit teams navigate internal management constraints and access to information challenges provides a more complete picture of what independence means in practice, and where reforms are most urgently needed.

Conclusions

Today, SAI independence is experiencing growing threats by indirect interference that quietly but persistently undermines their capacity to function. These pressures, manifested in budgetary restrictions, limits on staffing and internal management, and obstacles to timely access to information, strike at the heart of SAI operations, weakening their ability to fulfil their mandate even when legal safeguards appear strong. Recognizing and addressing these forms of interference is therefore as important as protecting SAIs from direct political pressure.

There is no single silver bullet to resolve these challenges. However, advancing stronger regulatory frameworks that guarantee long-term budgetary stability and give SAIs greater freedom to manage their teams is indispensable to secure their operational independence. At the same time, strengthening access to timely and complete information is crucial. The ongoing digitalisation of government data offers a promising opportunity: rather than depending on the delivery of specific documents, SAIs can be granted secure access to entire databases. This shift has the potential to enhance the efficiency, comprehensiveness, and timeliness of audits while closing avenues for indirect interference through obstruction or delay.

Works Cited

- Blume, Lorenz, and Stefan Voigt. 2011. “Does organizational design of supreme audit institutions matter? A cross-country assessment.” European Journal of Political Economy 27 (2): 215-229.

- Bouckaert, Geert , and Vital Put. 2016. “Managing Performance and Auditing Performanc.” In The Ashgate Research Companion to New Public Management (eBook), by Tom Christensen and Per Lægreid, 223-236. London: Routledge.

- Dye, Kenneth M., and Rick Stapenhurst. 1998. “Pillars of Integrity: The Importance of Supreme Audit Institutions in Curbing Corruption.” sirc.idi.no. https://sirc.idi.no/document-database/documents/development-partner-publications/43-pillars-of-integrity-the-importance-of-supreme-audit-institutions-in-curbing-corruption/file.

- Fredriksen, Camilla. 2023. “Global SAI Stocktaking Report 2023.” idi.no. https://idi.no/elibrary/global-sai-stocktaking-reports-and-research/2001-global-sai-stocktaking-report-2023-english/file.

- INTOSAI. 1977. “INTOSAI-P 1 The Lima Declaration.” sirc.idi.no. https://sirc.idi.no/document-database/documents/intosai-publications/1-intosai-p-1-the-lima-declaration/file.

- —. 2007. “INTOSAI-P 10 Mexico Declaration on SAI Independence.” sirc.idi.no. https://sirc.idi.no/document-database/documents/intosai-publications/2-intosai-p-10-mexico-declaration-on-sai-independence/file.

- OISC/CPLP. 2023. “Sumario Executivo. Áreas protegidas: auditoria coordenada.” agora-parl.org. https://agora-parl.org/sites/default/files/palop-publications/web-Sumário%20Executivo%20ACAP_v09.pdf.

- OLACEFS. 2019. “Auditoría Iberoamericana sobre el Objetivo de Desarrollo Sostenible 5: Igualdad de Género.” olacefs.com. https://olacefs.com/gtg/wp-content/uploads/sites/12/2021/12/04-00-Informe-ODS-5-ESP.pdf.

- Pierre, Jon, and Jenny De Fine Licht. 2017. “How do supreme audit institutions manage their autonomy and impact? A comparative analysis.” Journal of European Public Policy 26 (2): 226-245.

- Pollitt, Christopher, and Hilkka Summa. 1997. “Reflexive Watchdogs? How Supreme Audit Institutions Account for Themselves.” Public Administration 313-336.

- Power, Michael. 2009. “The Theory of the Audit Explosion.” Em The Oxford Handbook of Public Management, de Ewan Ferlie, Laurence E. Lynn e Christopher Pollitt, 326–344. Oxford University Press.

- Prasad, Awadhesh. 2018. “Environmental Performance Auditing in the Public Sector.” taylorfrancis.com. 13 de June. https://doi.org/10.4324/9781351273480.