Strengthening SAI Independence: Global Progress and the Saudi Experience

By Ms. Areej Mousa Aljehani, General Court of Audit, SAI of the Kingdom of Saudi Arabia

Introduction

Supreme Audit Institutions (SAIs) are pivotal in safeguarding public resources, ensuring that governments are held accountable and fostering transparency in the management of public funds. A key to fulfilling this role is their independence from undue external influence, which allows them to perform audits with objectivity and credibility. As emphasized by INTOSAI’s guidance, SAIs operate most effectively when shielded from interference, allowing them to properly strategize, acquire necessary information, and report findings without restrictions (INTOSAI, 2019). Political influence, budgetary constraints, and limited access to records can undermine audit quality and public trust. This article examines how the General Court of Audit (GCA) of Saudi Arabia has successfully navigated challenges to its independence through robust legal frameworks and disciplined execution, offering practical insights that other SAIs can adopt to reinforce independence and thereby enhance governance and public confidence.

Strengthening Independence: Saudi Arabia’s General Court of Audit (GCA) Reforms

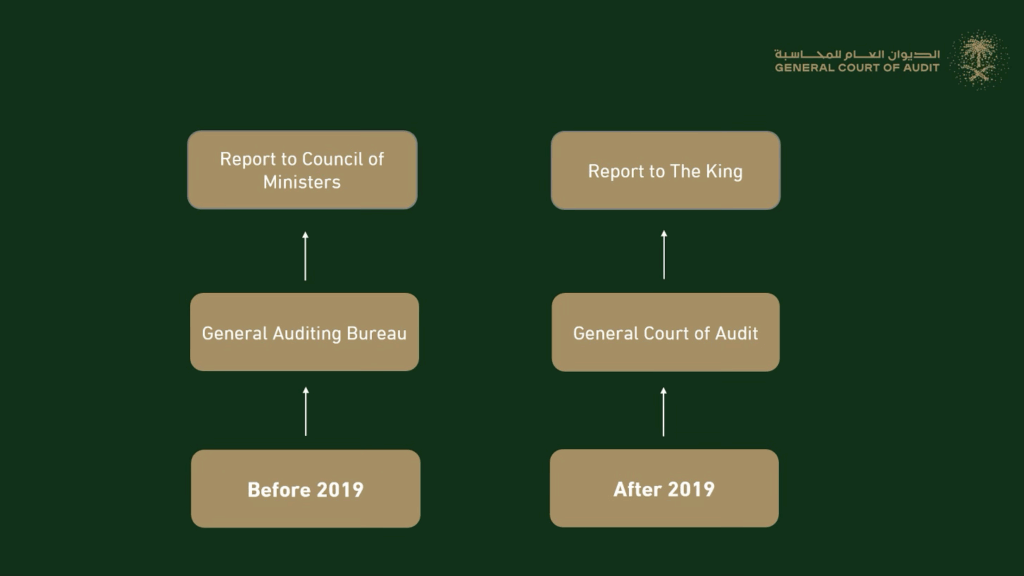

Prior to 2019, GCA operated under a governance and financial framework where it reported to the Council of Ministers, with leadership appointments requiring both ministerial decision and royal endorsement. However, without a clearly established audit framework, the GCA’s ability to systematically plan and prioritize audits was constrained. Resource allocation followed centralized budgeting channels, which posed a risk in GCA’s ability to plan and operate independently. While functional, this structure exposed the institution to public influence, making its work vulnerable to external pressures.

Significant reforms were introduced with the issuance of a Royal Decree in 2020, which shifted leadership appointments to the King. This marked a major governance change, reducing political influence and strengthening operational autonomy. Key provisions included royal appointment of the President and Vice President, and financial and administrative independence allowing the President to prepare the organizational structure, budget, and bylaws for royal approval. These reforms aligned GCA with INTOSAI-P 10 principles (INTOSAI, 2019), embedding independence into law and translating statutory protections into daily operational practice.

Operational Independence in Practice

Independence in Saudi Arabia is not only statutory, but also operational. GCA’s mandate guarantees unrestricted access to records, backed by legal consequences for non-compliance. It also provides authority to escalate unresolved issues to the highest executive levels, ensuring accountability, while direct reporting to the King strengthens institutional safeguards against interference. Between 2020 and 2025, these protections enabled audit teams to conduct procedures free from undue influence, significantly improving the quality and frequency of audit reports.

In daily operations, the legal framework and institutional practices ensure seamless access to necessary records and clear consequences when auditees resist cooperation. GCA can submit reports to the highest authority and engage with auditees to address findings, escalating issues when unresolved. This combination of legal safeguards and operational protocols converts statutory independence into effective practice, safeguarding objectivity, protecting public resources, and advancing the GCA’s vision to pioneer excellence in public auditing.

Nevertheless, institutional pressures that are inherent during the conduct of an audit persist. Auditees often prefer cooperative rather than critical assessments. GCA has responded by anchoring its work in international benchmarks, aligning with International Standards of Supreme Audit Institutions (ISSAIs) and International Standards on Auditing (ISAs) to guarantee objectivity. It has also invested in specialized expertise in information technology (IT) systems, financial assets, and contract reviews, equipping teams to handle complex audits confidently. Transparency has been enhanced through reporting to the King, and GCA has maintained constructive dialogue with ministries while making clear that final audit judgments rest solely with the institution. For example, audits of privatization programs and large-scale infrastructure projects placed particular emphasis on procurement transparency, asset valuation, and contract compliance. Even when politically sensitive findings were reported with clarity, reinforcing GCA’s credibility as a neutral guardian of public funds.

Practical Insights for Strengthening SAI Independence

Saudi Arabia’s experience demonstrates that independence must be embedded in law but also sustained in daily practice, meaning access to information, expertise, and tools is essential. Legal reforms such as explicit mandates, clear reporting lines, and safeguarded leadership appointments provide the foundation, but these must be reinforced by financial and administrative autonomy to protect internal decision-making.

Operational independence is equally critical, requiring guaranteed access to records, technical expertise to manage complex audits, and transparent reporting to the highest levels of government and the public. Transparency enhances credibility, while constructive engagement with audited entities can strengthen independence, it is imperative that the SAI retains full and unequivocal control over the reporting of its findings, without any interference in the material content of its reports. Perhaps most importantly, adaptability is key: as governments reform, SAIs must evolve their methods and capabilities to remain relevant and credible.

Building on this foundation, GCA has proactively engaged in international peer networks, including INTOSAI and INTOSAI Development Initiative (IDI) initiatives, as part of its own strategy to strengthen independence. Through these engagements, GCA has benchmarked its legal, financial, and operational safeguards against global best practices and adapted lessons to its domestic context. The institution has benefited from exchanging experiences with other SAIs, learning how to manage challenges such as political pressure, budgetary constraints, and sensitive audits. These interactions have enhanced the GCA’s credibility and operational autonomy, reinforced its de facto independence, and provided access to technical guidance, frameworks, and tools that complement domestic reforms. By integrating insights from global networks into its own practices, GCA has turned international engagement into a concrete, practical mechanism for sustaining and strengthening its independence.

Conclusion

Independence is not a single reform but an ongoing process. The experience of Saudi Arabia’s General Court of Audit shows that legal safeguards, operational autonomy, and strong institutional practices must work together to make independence a practical reality. By establishing clear mandates, protecting leadership appointments, and ensuring robust budgetary frameworks and transparent reporting, GCA has strengthened its ability to audit without interference and safeguard public resources. Its proactive approach, including specialized expertise and engagement with international peer networks, demonstrates how practical measures can reinforce independence in both law and practice. This experience shows that SAI independence is strongest when legal, institutional, and operational measures work together to ensure accountability and public trust.

References

- Bureau of Experts (Kingdom of Saudi Arabia). Law of the General Court of Audit (as amended by Royal Decree No. M/178 dated 2/12/1441H). Riyadh: Bureau of Experts, 2020. https://laws.boe.gov.sa/BoeLaws/Laws/LawDetails/5dc538d4-5bbd-4995-8f0c-a9a700f2c88c/1?utm_source.

- General Court of Audit (Kingdom of Saudi Arabia). Introductory Brochure. Riyadh: GCA, 2020. https://www.gca.gov.sa/uploads/documents/Introductory.brochure.pdf

- International Organization of Supreme Audit Institutions (INTOSAI). INTOSAI-P 10: Mexico Declaration on SAI Independence. Vienna: INTOSAI, 2019. https://www.intosai.org/fileadmin/downloads/documents/open_access/INT_P_1_u_P_10/INTOSAI_P_10_en_20….